Stephen T. Parente, Jessica Haupt, and Molly Dube, University of Minnesota

Contact: paren010@umn.edu

Abstract

What is the message? The Medical Valuation Laboratory, part of the University of Minnesota’s Carlson School of Management and its Medical Industry Leadership Institute (MILI), conducts rapid market assessments for new medical innovations. Data from these assessments show that structured, early-stage business and market evaluation meaningfully predicts which medical innovations are most likely to succeed commercially. The Valuation Lab’s “proceed/invest” recommendations are not just pedagogical exercises; they are systematically associated with stronger downstream outcomes, suggesting that disciplined translational assessments can accelerate promising innovations while steering resources away from weak ones.

What is the evidence? Using more than 500 Lab projects evaluated since 2008 and follow-up survey and market data, the authors show a strong positive association between favorable Lab recommendations and subsequent capital raised, ROI potential, and commercialization progress. Innovations receiving “Proceed” or “Invest” recommendations raised substantially more capital and generated dramatically higher aggregate returns than “Do Not Invest” projects. Patterns were consistent across technology types, stages, and time, reinforcing the predictive value of structured evaluation in translational medicine.

Timeline: Submitted: September 25, 2025; accepted after review January 21, 2026.

Cite as: Stephen T. Parente, Jessica Haupt, Molly Dube. 2026. Uncovering Barriers to Translation: Findings from the Medical Valuation Laboratory. Health Management, Policy and Innovation (www.HMPI.org). Volume 11, Issue 1.

Introduction

The University of Minnesota’s Carlson School of Management and its Medical Industry Leadership Institute (MILI) are recognized leaders in business education and research. MILI offers students innovative training, knowledge, and experience through industry-specific courses and unique hands-on learning[1]. In 2008, MILI started the Medical Valuation Laboratory, which has grown to be the signature program from the perspectives of business partners, inventors, and students.[2] The Medical Valuation Laboratory conducts rapid market assessments for new medical innovations. The students in the course analyze over 30 analyses per year, helping assess lifesaving ideas and streamlining the time-to-market for critical new products. Since 2008, more than 500 innovations have come through the Lab. These innovations have been sourced from organizations and individual inventors throughout Minnesota, across the nation, and around the globe. Each analysis concludes with a binary recommendation to the investor to invest or not as well as the inventor where students suggest whether they should continue to pursue the innovation.

In this paper, we survey the inventors examined by the Lab since 2008 to analyze any correlations between the Lab’s recommendations and the outcome of innovation in terms of market development. We find the Lab’s investor recommendations are suggestive of future success. There is a strong correlation between positive recommendations and capital raised, reinforcing the importance of structured evaluation processes.

Background

The origins of the Medical Valuation Laboratory began with repeated calls from industry to MILI leadership to identify novel mechanisms to speed University assessments of medical innovations from clinical research to be translated into new products. Working in cooperation with the University of Minnesota’s Office of Technology Commercialization, MILI faculty sought to design a course where MBA students as well as graduate and professional students from different colleges and with different levels of expertise could provide ‘another set of eyes’ to relieve the backlog of projects at the University. The experimental course went into ‘production mode’ in the fall of 2008, with a defined client/inventor intake process and outputs in the form of white paper and PowerPoint presentation to the inventor.

Clients seeking the Lab’s top-to-bottom analysis of their technology and its market prospects, are from the University of Minnesota, single entrepreneurs, hospitals and clinics, medical device manufacturers, healthcare startups, nonprofits, and more. Once a project is accepted into the Lab, students from nine different colleges at the University of Minnesota can enroll in the course to gain hands-on, real-world experience. Organized into interdisciplinary teams, students take five weeks to complete a full and thorough evaluation of the innovations by appling a business framework. They research market size/potential, competition, intellectual property, regulatory analysis, technical and user evaluations, and finance/reimbursement. Students then develop a recommendation advising both the inventor and potential investors on the feasibility of proceeding with the innovation.

Methods

We examined over 500 projects completed by the Valuation Lab since 2008. We sought to identify common barriers hindering inventors from transitioning their ideas into viable products available to patients. We used the data from the project reports and white papers as well as recommendations to discover if there are recurring themes influencing the process. Several questions drove our investigation:

- Would the data show us themes in the innovations that were successful?

- Are there common points of delay in projects that received a “do not to proceed” recommendation? If so, what are those gaps and how can we address and support them through education, training, and mentorship?

Providing targeted support to help inventors effectively navigate and mitigate roadblocks during the initial development stages, could accelerate the process of getting potentially lifesaving innovations to patients. By summarizing our research and offering recommendations for training, we envisioned a tangible impact on expediting the translation of groundbreaking medical innovation discoveries into life-saving interventions.

We then sent a survey to the inventors of the innovations examined by the Laboratory to assess whether our predictions of “do or do not invest” as well as “do proceed or do not proceed” were associated with the subsequent success of the innovation. Our response rate was 28%, not very robust for statistical inference. However, much of the contact information and innovation branding to achieve a higher response rate was either lost or not pursued.

Our methods include two main components. First, we identify common themes where recommendations advise against proceeding with commercialization efforts. By examining the research behind these recommendations, we sought to uncover recurring barriers such as market size concerns, regulatory hurdles, intellectual property challenges, or inadequate technical validation. Second, we examined the factors underpinning the success of innovations that receive positive recommendations. By recognizing patterns among these success stories, we can create actionable plans that can inform and guide future inventors toward more favorable outcomes. These insights may encompass aspects such as market demand, effective intellectual property strategies, strategic partnerships, or alignment with unmet clinical needs. In addition, we leveraged resources to correlate project data with Pitchbook or DUNS information to track project progress, funding acquisition, and employment growth. Overlaying this data with Valuation Lab recommendations enabled us to identify potential correlations and trends. Finally, we conducted surveys of Lab clients to compare our findings and recommendations with actual project outcomes.

Our data originate from a wide range of projects – from device to biologics to oncology and cardiac. They also come from a wide range of locations – from Minnesota to California, from Sweden to Cambridge in the United Kingdom. We therefore believe that our research and findings can be adaptable and potentially establish generalizable principles for accelerating translational science across the healthcare spectrum and around the globe. After identifying the barriers, and by providing a framework to acknowledge common translational obstacles, our project allows for inventors to be aware and apply our principles in ways that are most relevant and impactful.

In summary, our work aims to establish generalizable principles for accelerating translational science by systematically identifying common barriers, developing potential solutions to the barriers, and sharing the knowledge with others. Through these efforts, we seek to assist inventors across diverse settings and areas of healthcare to overcome translational challenges and expedite the translation of discoveries into real-world solutions that improve human health and well-being.

Results

Our results are organized into three sections. First, we describe the relationship between the Lab’s recommendations and capital the inventors have raised for their innovations. Second, we decompose the differences by the types of technologies and success with capital acquired for the innovation. Third, we summarize the temporal trends we identified over that period with respect to investment decisions and capital invested.

Projects that received a positive Investor Recommendation (“Invest”) were strongly associated with higher capital raised. On average, projects recommended for investment attracted significantly more funding than those marked “Do Not Invest”. A positive correlation coefficient in technology categories (e.g., device, software) between the numeric investment recommendation score and capital raised, supports a moderate positive relationship and implies that expert evaluations influence or reflect the likelihood of successful capital acquisition.

Three additional insights were: 1) “Invest” recommendations had the highest mean capital raised and a wider distribution, suggesting a mix of both high-potential ventures and outliers; 2) projects labeled “Do Not Invest” received little to no funding, confirming alignment between investor skepticism and market reception, and 3) “Further Info Needed” cases showed more variable outcomes, reflecting some uncertainty in the evaluation process.

Projects in the Device category saw the highest average capital raised, indicating strong investor and market interest in tangible medical innovations. In contrast, categories like Digital Health and Service showed lower average capital, possibly reflecting either earlier-stage development or more competitive funding environments.

Projects at the Pre-Market stage surprisingly received more capital on average than those at Post-Market stage. This may reflect significant early-stage investments required for clinical development, prototyping, and regulatory approval before revenue generation.

With respect to temporal trends, capital raised has shown fluctuations across years, with notable spikes during select periods, possibly influenced by macroeconomic cycles, policy incentives, or lab focus shifts. The accompanying bar chart shows capital raised per year and highlights growth in certain years that may warrant further investigation.

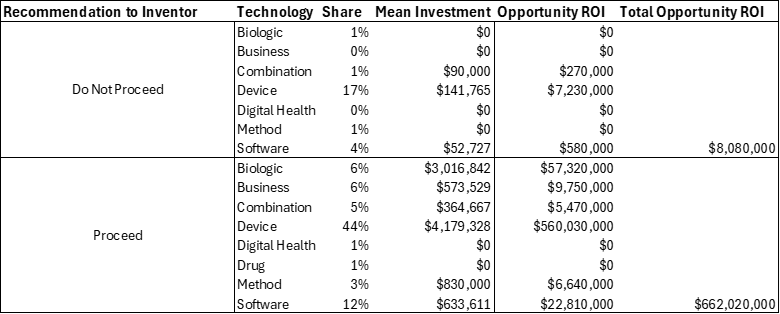

Table 1 describes the potential return on investment (ROI) for the “Proceed” recommendation to the inventor. The table compares two categories of technology investment decisions: those recommended “Do Not Proceed” versus those that were advanced under “Proceed.” In the “Do Not Proceed” group, 71 technologies were considered, with very modest mean investments of about $40,600 each and a total estimated opportunity ROI of only $8.1 million. In contrast, the “Proceed” group contained 236 technologies, each requiring a far greater mean investment of roughly $1.2 million but generating an enormous cumulative ROI potential of $662 million. This highlights a stark difference in both scale and outcomes between the two approaches.

Table 1: Return on Investment (ROI) Opportunity from Val Lab Proceed Recommendation

Although declining to proceed limited exposure to upfront costs and investment risk, the foregone opportunity value was significant. Advancing technologies required much larger financial commitments but ultimately yielded vastly higher returns, demonstrating the economic advantage of pursuing development. In essence, the “Proceed” strategy provided an ROI nearly 80 times greater than the alternative, indicating that, despite higher resource demands, the decision to proceed proved far more effective in generating financial value.

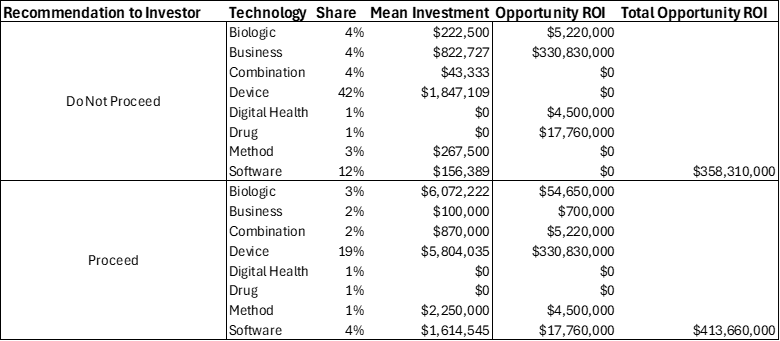

In contrast, Table 2 describes the potential (ROI) for the “Invest” recommendation to the inventor. The table compares outcomes under two recommendations: not to invest and to invest across various technology categories (biologics, devices, digital health, software, etc.). Under the “Do Not Invest” recommendation, the total opportunity ROI summed to approximately $358.3 million, while under the “Invest” recommendation the total was higher, at about $413.7 million. This shows that both strategies generated substantial returns, but the distribution of investments and their mean size differed. The “Do Not Invest” recommendation leaned on lower per-project investments with a few outsized returns, while the “Invest” recommendation concentrated larger investments across broader categories, including devices and software.

Table 2: Return on Investment (ROI) Opportunity from Val Lab Invest Recommendation

Interpreting the totals, the recommendation to invest produced a better overall ROI compared to not investing, with roughly a $55 million advantage. This suggests that taking on more projects and deploying capital more broadly yields higher aggregate returns. While not every individual investment category within the “Invest” set showed positive outcomes, the broader spread of investments captured enough high-performing opportunities (notably in devices and software) to outweigh weaker areas. Overall, the recommendation to invest was superior in ROI terms, demonstrating that a more aggressive capital deployment strategy across multiple technologies paid off better than holding back.

Lessons Learned for Future Translation

The journey of early-stage ventures provides valuable lessons for investors, particularly when reviewing a diverse set of founders and project outcomes. The following synthesis distills key insights from founders and innovators, highlighting the successes, setbacks, and pivots that shaped their paths. For investors, these reflections offer practical guidance on evaluating opportunities, anticipating risks, and understanding the lived realities of innovation.

One of the most common themes relates to intellectual property (IP) management. Several ventures pursued patent protection but ultimately abandoned applications after receiving feedback that weakened their prospects. For example, one founder noted, ‘A patent application was filed and also abandoned after feedback,’ while another concluded, ‘Final patent renewal due now, not renewing.’ These experiences illustrate that while patents can serve as important assets, they also require careful cost-benefit analysis. Investors should recognize that sunk costs in IP do not always justify continued investment if market validation or novelty is lacking.

Conversely, some ventures achieved progress with patents, including published applications that contributed to credibility and potential valuation. The lesson is that investors should carefully probe the IP strategy of startups—ensuring that patent pursuits align with broader commercialization goals rather than standing alone as markers of success.

Regulatory approval often defines the pace and scale of growth, especially in medical and health-related fields. Comments highlighted milestones such as, ‘Approved by FDA and market launched,’ and ‘FDA cleared on primary device, working on further claims.’ These achievements demonstrate both the potential value of regulatory clearance and the long, resource-intensive process leading up to it.

However, delays and shifting requirements can derail projects. Several founders referenced the time and expense tied to pursuing additional claims or extending regulatory coverage. Investors should anticipate these cycles and ensure portfolio companies are adequately resourced to navigate them.

A number of projects benefited from non-dilutive financing such as SBIR (Small Business Innovation Research) grants. One team shared, ‘Currently on our 3rd funded SBIR project from NIH.’ These examples highlight the importance of grant funding as both a validator of scientific merit and a mechanism to extend runway. Yet other comments revealed financial fragility. Ventures noted abandonment due to personal circumstances, COVID-19 disruptions, or lack of capital. Investors should weigh not only technological promise but also the team’s capacity to secure sustainable funding and weather external shocks.

Startups frequently recalibrated their business models. As one founder wrote, ‘We added B2B software for practitioners soon after,’ signaling a pivot from a direct-to-consumer focus toward a more viable business-to-business model. Others described adding features or altering their commercialization strategies in response to feedback. These pivots underscore the importance of agility. Investors should view pivots not as red flags, but as potential signals of responsiveness and market learning—provided that the changes are grounded in evidence rather than desperation.

The comments also capture how external shocks impact venture trajectories. The COVID-19 pandemic, for example, forced one team to halt progress entirely: ‘Due to Covid and personal issues, the project ended.’ Similarly, competition posed existential threats, as when students uncovered that another company had already developed a similar innovation.

For investors, these examples reinforce the importance of diversification and resilience planning. Even the most promising ideas can falter in the face of unexpected global or competitive dynamics. Partnerships with leading institutions surfaced as pivotal milestones. Examples include projects conducted ‘At Mayo Clinic and Mt. Sinai,’ signaling credibility and validation. Likewise, acquisitions provided tangible outcomes: ‘Acquired by international medical device maker.’ Such exits and collaborations illustrate that successful outcomes are not limited to independent commercialization. For investors, partnership-readiness and strategic alignment with established players can serve as leading indicators of future value.

The collective lessons highlight the complexities of early-stage innovation. Investors must balance optimism with diligence, recognizing the trade-offs in patent strategy, the unpredictability of regulatory pathways, the importance of non-dilutive funding, the inevitability of pivots, the risks of external shocks, and the value of partnerships. While not every venture achieves FDA approval or acquisition, each contributes insights that sharpen investor judgment. By internalizing these lessons, investors can more effectively evaluate opportunities, manage portfolio risk, and ultimately support the translation of innovation into impact.

Implications and Summary

There are three major takeaways from this analysis. First, the Lab’s recommendations are more often correct than not. There is a strong correlation between positive recommendations and capital raised, reinforcing the importance of structured evaluation processes. This finding demonstrates that the comprehensive approach used by the Lab is effective at identifying early innovations that have the potential for significant return on investment.

Second, we find that early-stage capital is concentrated. A significant portion of funding goes into early-stage or pre-market projects, which underscores the need for robust pre-commercialization support and risk management. It is unsurprising that early investment in successful innovation tends to deliver significant multiplier returns for investors, compared to those who invest at later stages when the technology is more established and market competition has increased.

Finally, the innovation category and time matter. Medical device innovations dominate funding, and the timing of entry into the ecosystem (year and stage) significantly impacts capital outcomes. We suspect this finding is associated by the significant barriers to entry for medical devices that need to be overcome for regulatory and reimbursement approval. Other technologies, for example digital health innovations, often have multiple competitors and weak revenue potential (compared to medical devices or pharmaceuticals) and a much smaller multiplier for investment in and financial reward out for institutional investors and venture capital.

Acknowledgements: This research was supported by the National Institutes of Health’s National Center for Advancing Translational Sciences, grant UM1 TR004405. The content is solely the responsibility of the authors and does not necessarily represent the official views of the National Institutes of Health’s National Center for Advancing Translational Sciences.”

References

[1] MBA programmes that create leaders in global healthcare. Study International. 12 Nov 2020. https://studyinternational.com/news/mba-programmes-that-create-leaders-in-global-healthcare/ Accessed January 15, 2026.

[2] MILI Valuation Lab: Carlson School Lab Influences Med Tech. University of Minnesota. October 13, 2023. https://carlsonschool.umn.edu/news/mili-valuation-lab-carlson-school-lab-influences-med-tech Accessed January 15, 2026.