Jocelyn J. Fitzgerald, Assistant Professor, Department of Obstetrics, Gynecology & Reproductive Sciences, Division of Urogynecology & Reconstructive Pelvic Surgery, University of Pittsburgh Medical Center, and Christina Vosbikian, Blavatnik Fellow in Life Science Entrepreneurship, Harvard Business School

Contact: cvosbikian@mba2025.hbs.edu

Abstract

What is the message? Obstetrics and Gynecology faces unique financial and structural challenges that undermine both providers and patients. Supply shortages, undervaluation of women’s health procedures, malpractice pressures, closing sites of care, and barriers to benefits from innovative investment have created unsustainable conditions. Because reimbursement structures and policy frameworks systematically disadvantage OB-GYNs, reform is needed to right-size payment, expand representation, and ensure women have access to essential care.

What is the evidence? The article explains how reimbursement for OB-GYN services is set, showing that female-specific procedures are consistently undervalued compared to male procedures. Budget neutrality rules likewise create tradeoffs between obstetrics and gynecology, leaving both undervalued. Workforce shortages are growing as providers leave due to liability risk, burnout, and declining salaries, especially as the specialty has become majority female. Many counties are now maternity care deserts, with no OB-GYNs or birthing facilities, which worsens outcomes for millions of women. Hospitals often close obstetric units because margins are low compared to other specialties. The authors outline potential reforms, including revisiting RVU standards, adding representation for gynecologic surgery in the RUC, adjusting Medicaid reimbursement to reflect access gaps, and separating reimbursement streams for obstetrics and gynecology.

Timeline: Submitted: July 30, 2025; accepted after review October 2, 2025.

Cite as: Jocelyn J. Fitzgerald; Christina Vosbikian. 2025. The Price of Care: Financial Pressures’ Ramifications on OB-GYNs and Patients. Health Management, Policy and Innovation (www.HMPI.org). Volume 10, Issue 2.

Introduction

The Obstetrics and Gynecology market seems to defy basic principles of supply and demand.

OB-GYN workforce shortages are intensifying[1],[2]. The American Congress of Obstetricians and Gynecologists (ACOG) projects a shortage of up to 22,000 physicians by 2050.[3] Today, the average wait time for an American woman to see an OB-GYN is 31 days[4] and OB-GYNs have 15 minutes on average for appointments with their patients, each seeing 30-40 patients per day.

Demand for OB-GYN services, on the other hand, is relatively sticky. Given this, in the face of such low OB-GYN supply and sustained high demand, we would expect the “cost” of OB-GYN services – reflected in OB-GYN compensation and hospital-generated revenues – to reflect an increase. We might then expect supply to increase with OB-GYNs staying in the market and new OB-GYNs entering, hypothetically improving conditions for providers and patients alike.

Of course, this hypothetical free market homeostasis is far from the reality, as is true in many medical specialties. Unlike other specialties, however, unique disadvantages faced by OB-GYNs add to reimbursement-driven difficulties for patients and providers alike.

Between the supply side – provider shortages and closing sites for care – and lagging demand for women’s health innovation, the business fundamentals of women’s healthcare have driven the system to a precipice.

The Foundations of OB-GYN Payment

The System of Reimbursement “Price Setting”

The current reimbursement system for healthcare services in the U.S. was established through the Omnibus Budget Reconciliation Act of 1989, which authorized the Medicare Resource-Based Relative Value System. The Medicare Physician Fee Schedule was then implemented in 1992, more formally assigning all medical procedures a unit of measure and value commonly referred to as a Relative Value Unit (RVU). The move to an RVU-based system represented one of the most wide-reaching reforms in payment since Medicare’s establishment in 1966 and came on the back of wide-ranging physician demand for uniformity in payment structure versus discretionary payment practices commonly employed up until that point[5].

The AMA’s Relative Value Scale Update Committee (RUC), established in 1991, advises CMS on the relative value of physician services for Medicare reimbursement. Each medical specialty’s society appoints a representative of their own to the RUC. OB-GYN is represented by a single appointee from ACOG[6]. As such, the OB-GYN seat reflects the interests of ACOG’s majority Obstetrician-Gynecologist membership. Specialty Gynecologic Surgery, which includes Gynecologic Oncology, Urogynecology, and Minimally Invasive Gynecologic Surgery, is structurally underrepresented. Physicians within ACOG note that Gynecologic Surgery is the only sub-specialty within the RUC without its own representation. This is important especially because reimbursement decisions and policy impact Obstetrics and Gynecology differently.

Calculating OB-GYN Procedures’ Value

There are three types of RVUs: 1) physician work RVUs (wRVUs); 2) practice expense RVUs (PE RVU); and 3) professional liability insurance RVUs. Without getting into the differences between facility and non-facility fees, the basic Medicare Fee Schedule rate formula is such that: Payment = [ (Work RVU * Work GPCI) + (PE RVU * PE GPCI) + (MP RVU * MP GCI) ] * CF

The Conversion Factor (CF) is a number that CMS sets every year, to account for overall cost of care fluctuations in a simple multiplier. The Geographic Practice Cost Index (GPCI) is a more specific multiplier that accounts for differences between geographies, applied to each RVU section. Services and payment for them are categorized under Current Procedural Terminology (CPT) codes, which are the individual codes per service that clinicians submit to insurance for subsequent payment.

Within this formula, wRVUs are often the biggest needle movers on final payment. To calculate foundational wRVUs, the Office of Health and Human Services (HHS) asked the Harvard School of Public Health to conduct a study “Estimating Physicians’ Work for a Resource-Based Relative-Value Scale” published in 1988, which accounted for time, mental effort, technical skill and psychological stress to determine RVUs via a Resourced-Based Relative Value Scale (RBRVS).[7] The new, RBRVS-based schedule was fully implemented by 1996. Some initial critique suggested that the new system “resulted in underpayment of office-based practice expenses and overpayment of hospital-based practice expenses.”[8]

The RUC uses annual surveys that are sent out by ACOG, asking a small percentage of their membership to evaluate the time and effort spent doing different procedures in order to reassess the appropriateness of their value. The most recently published data showed that 10% of ACOG’s membership responded to the surveys. Sending the survey to ACOG as a whole creates the dynamic whereby members, most of whom are not subspecialist Gynecologic surgeons, are asked to evaluate the sub-specialty’s work. This makes it especially difficult to surface conversations about Gynecologic surgeries like endometriosis excision or vaginal reconstruction to the negotiating table[9].

Foundational Rate Setting Disparities in OB-GYN

As outlined by Dr. Rosa Polan and Dr. Emma Barber[10], studies of initial rate setting from as early as 1997 show that sex-specific procedures for women are undervalued and poorly reimbursed, without any surgically justifiable reason for this disparity[11].

More recent work “Price and Prejudice: Reimbursement of surgical care on male vs. female anatomies” published in 2024[12] shows must of the same:

- Significantly Lower RVUs for Female-Specific Procedures: Among the procedures analyzed, RVUs were, on average, 30% higher for male procedures, with some disparities reaching as high as 142.8%.

- Lower Reimbursements in Facilities: In facilities, procedures on male patients often received reimbursements averaging 25.6% more than those for female patients. For example, reconstruction of the urethra was reimbursed at a maximum difference of $772.96 more for males than females.

- Greater Disparity in Minor Procedures: Minor procedures on female patients were particularly undervalued, with 84% of these procedures receiving significantly lower RVUs than equivalent male procedures.

- Differences in Urinary Tract Procedures: For urinary tract procedures, 75% of those performed on male patients received higher RVUs and reimbursement rates, averaging 49.1% higher than those for females.

- Stagnation in Reimbursement Progress: Between 2003 and 2023, there was no statistically significant progress in closing these gaps, meaning male-specific procedures consistently received an average RVU 31-34% higher than female-specific procedures.

Zero Sum Gain in Obstetrics and Gynecology

The other critical context to understanding OB-GYN reimbursement is the establishment of budget neutrality, which was written into the Omnibus Budget Reconciliation Act of 1989. This required that changes to the physician fee schedule not increase total Medicare spending by more than $20 million, a number that has not been changed since despite physician advocacy for an increase[13]. In the years that followed the original implementation of the physician fee schedule, CMS implemented budget neutrality by reducing work RVUs across all services. This is particularly important for OB-GYN, because if one procedure is determined to require an increase in relative value (RVU), then the relative value of other procedures must go down.

Polan and Barber illustrate the practical application of this point in women’s health:

Effective January 1st, 2021, the Centers for Medicare and Medicaid Services increased the relative value of evaluation and management billing codes. Because of mandated budget neutrality, meaning Medicare expenditures cannot significantly increase or decrease from year to year, this change necessitated a reduction in the reimbursement of surgical procedures. The work relative value units (RVUs) assigned for procedures did not change; however, the dollars per RVU decreased. As a result, Obstetrics and Gynecology was projected to have an 8% increase in payments. This is because Obstetric care is paid for using global codes, meaning labor and delivery, prenatal, and postpartum office visits are paid for using a single code, valued at evaluation and management billing rates. However, if an obstetrician-gynecologist derives most of their income from gynecologic surgical procedures, they are likely to experience a 7% decrease in reimbursement, as these changes in evaluation and management billing rates do not apply to global surgery codes.

This dynamic has led many to advocate for a delineation of specialties, with Drs. Jocelyn J. Fitzgerald, MD, URPS, FACS, and Louise P. King, MD, JD, FACS, writing: “…the health needs of the female public cannot sustain a budgetary competition between Obstetrics and Gynecology when both are severely undervalued in terms of revenue generation.”

Other providers, like Dr. Lyndsey Harper, MD, FACOG, also note that OB-GYNs should be at the negotiating table when Purchasing Organizations – who often manage contracts even for private OB-GYN practices – are working with payors to set rates at systems where OB-GYNs are working, with little transparency.

The Difficult Business of OB-GYN Care

With a high-level understanding of the OB-GYN reimbursement policy history, we may consider how recent market dynamics layer on to payment trends to uniquely exacerbate current challenges faced by OB-GYNs and, in turn, their patients.

Provider Supply: Fixed Legal Costs and Salary

As of 2021, HRSA estimated that between 2018 and 2030, there would be a 4% increase in demand for OB-GYN services and a 7% decrease in supply. They estimated this would result in a projected overall deficit of 5,170 full-time OB-GYNs nationwide by 2030[14].

These shortages are, in some ways, not unlike shortages in Primary Care and other specialties, where an aging workforce and mountains of paperwork loom ahead of once-hopeful students with an interest in the medical field.

However, in other ways, OB-GYN burnout and the difficulty in practicing in the field stands out. OB-GYNs join general surgeons with the highest number of liability claims, according to an AMA study[15]. Malpractice rates have, unsurprisingly, risen steeply as vague abortion bans have been introduced in certain states. Post-Dobbs restrictions have created new, massive risk for lawsuits and, often, even jail time for OB-GYNs who deliver healthcare to their patients. This has created difficult situations where providers, at the fear of being jailed and sued, do not perform necessary healthcare procedures on patients – leading to increases in near-death hemorrhage for women experiencing miscarriages in Texas[16], for example. All in all, surveys suggest 30% of OB-GYNs stop practicing obstetrics – despite it being more highly reimbursed than gynecology – within 12 years of practice, citing malpractice insurance costs as a primary factor[17].

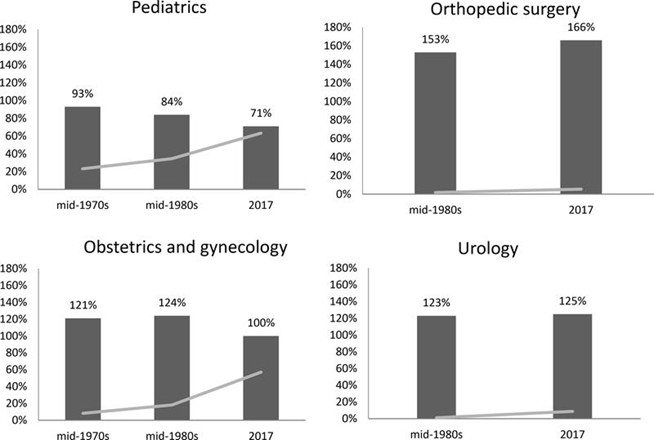

Other factors, such as provider compensation, in the largely female field of OB-GYN also play a role in the unique shortage we see. Pelley and Carnes[18] outline this:

The salaries in obstetrics and gynecology were 20% to 25% higher than the mean physician salary in the mid-1970s and 1980s when the female share was 8% and 18%, respectively. However, by 2017 with a female share of 57%, an obstetrician/gynecologist became an average physician earner. In contrast, urology, earned 123% of the average physician salary in the mid-1980s when it was 1% female and 125% of the average salary in 2017 when the female share rose but was still low at 9%.

This work also cites a 20% decline in salary relative to the average physician seen in the two most female-predominant specialties, Pediatrics and Obstetrics and Gynecology, over the past four decades.

Normalized Average Physician Salary vs. Share of Female Physicians

Note: Dark bars show specialty’s average salary relative to median at the time; gray lines show share of female physicians over time.

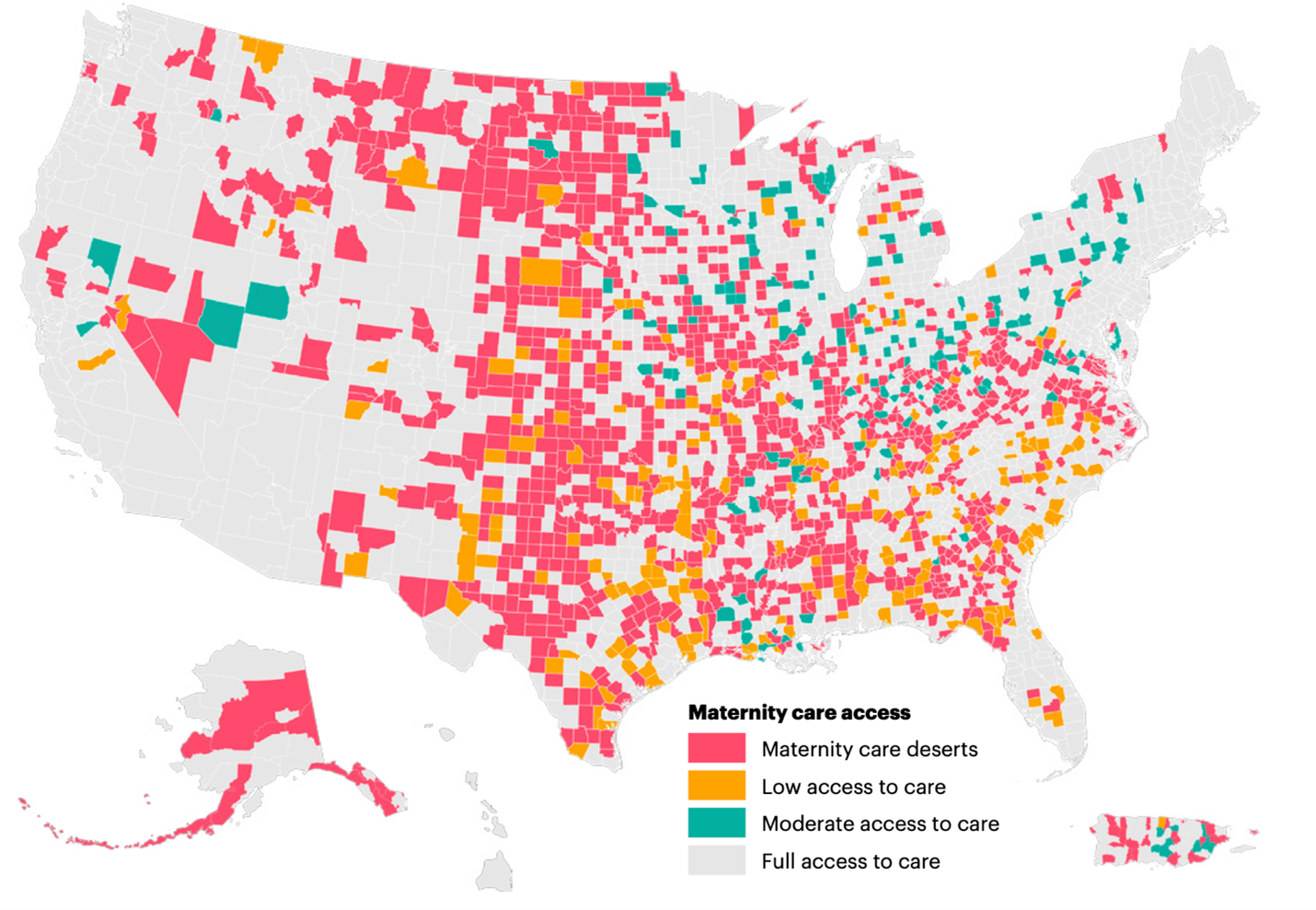

Closing Sites of Care

March of Dimes reported that 35% of U.S. counties are considered maternity care deserts, with no birthing facility or obstetric clinician and that over half of counties do not have a hospital that provides obstetric care.[19] This leaves more than 2.3 million women of childbearing age in the U.S. living in a county where there are no OB-GYNs, birthing centers or hospitals that deliver babies. March of Dimes’ report shows that “ women living in maternity care deserts and counties with low access to care have poorer health before pregnancy, receive less prenatal care, and experience higher rates of preterm birth.” These are often in rural areas[20].

Reasons are reported as a mix of declining birthrates, lack of providers, increased costs and comparatively low revenue versus other specialties. With hospitals facing razor-thin margins, it is not unsurprising that management teams would look to prioritize higher-revenue departments. For example, the table below exhibits what a hospital might gain by prioritizing other non-gynecological surgical care.

| Procedure |

Specialty/Training Time |

Time to complete by high-volume surgeon |

wRVU |

wRVU / Hour |

| Sacrocolpopexy (complex laparoscopic or robotic vaginal reconstruction) |

Urogynecology

7 years |

3-4 hours |

17.03 |

4.87 |

| Complex Hysterectomy >250 grams |

Minimally Invasive Gynecologic Surgery

6 years |

2-4 hours |

20.06 |

6.69 |

| Radical Hysterectomy with lymph node dissection |

Gynecologic Oncology

7-8 years |

3-5 hours |

30.91 |

7.73 |

| Endometriosis excision |

Minimally Invasive Gynecologic Surgery

6 years |

1-8 hours (if significant frozen pelvis/disease invasion) |

12.15 |

2.70 |

| Shoulder arthroscopy |

Orthopedic Surgery

5-6 years |

30 minutes-1 hour |

15.59 |

20.79 |

Note: wRVUs are illustrative (calculated as wRVU / mean time to complete), for ease of comparison.

Demand for Women’s Health Innovation

Though venture capital investment in women’s health has tripled between 2019 and 2024[21], there is a long way to go before positive feedback loops cement enthusiasm for building up the space. There are many reasons for this, including historical under-representation of women as decisionmakers in scientific and capital-allocating authorities. Other reasons include a relative lack of exits[22] – and thus lacking a track record of making financial returns – in the space, whether in medical devices, care delivery, healthcare IT / services or therapeutics. Of course, this is unsurprising given the space is so “new” – but it lends to a persisting view of women’s health investing as a money-losing game.

This shows up in patient care. Dr. Harper notes that, if a patient has endometriosis and wants a new endometriosis drug, that patient’s physicians must prescribe that patient a traditional birth control regimen, regardless. Only with a track record of failing the standard, likely less expensive treatment – even if the patient’s physician knew this regimen would likely not work for their patient – is the new, more effective drug likely to be approved by the patient’s insurance company.

While this type of cost-control is familiar across many medical specialties, it is especially damaging in women’s health, where a drug may represent a pharmaceutical company’s first-ever investment in a female-specific condition. If their sales are stagnant because of likewise new and changing prior authorization requirements, it creates an especially harmful negative feedback loop against any future women’s health investment.

The same holds for non-life science investors, like Private Equity or Venture Capital, when or if they decide to invest in women’s health. If overall especially difficult market dynamics in an early market push early players into capital impairment, firms are unlikely to put more money to work in the next women’s health companies that come to market.

Policy Reform and the Road Ahead

With uncertainty in Medicaid – which covers more than two out of five births – continued shifts in post-Dobbs legislation, and more, the road for women’s health providers, patients, and innovators is likely to be rocky for the foreseeable future.

That said, there are key steps forward we should prioritize that could promise to reform parts of the system, specifically: 1) under-reimbursement in Gynecology versus comparable male-focused procedures and related reimbursement tension between Gynecology and Obstetrics; 2) shortages and downstream lagging patient outcomes in Obstetrics; 3) RUC-focused adjustments that would benefit both Obstetrics and Gynecology.

To address the relative under-reimbursement in Gynecological procedures specifically versus other specialties and inherent tension between Obstetrics and Gynecologic service reimbursement, Dr. Fitzgerald aptly outlines that policymakers and advocates might:

- Re-evaluate RVU Standards: Advocacy for studies to reestablish fair reimbursement standards for gynecologic surgeries, led by relevant professional groups. There is no reason to believe that Gynecologic services are less complex than other surgical services. A re-issued survey of physician work using empirical time-based data such as time-motion studies could be a first step in codifying this and re-establishing correct relative work measures versus the more qualitatively-rooted surveys that were originally established and are still in-use.

- Pursue policy and legislative action: Engaging government agencies like the CMS, the Secretary of Health, and members of Congress to review and revise existing policies, particularly the budget neutrality clause and the composition of the RUC to include a seat for Gynecologic Surgeons. Explore legal recourse under the Affordable Care Act and the 14th Amendment, with the aim of addressing potential gender-based discrimination in healthcare reimbursement.

To address the acute shortages in Obstetrics care, we offer different policy considerations. Given Obstetrics services are not generally provided to the Medicare population – there may be a strong case for moving towards more bespoke measures to account for the current provider shortages and lagging outcomes in Obstetrics.

One consideration is whether state payors might include network adequacy measures when setting prices for Obstetrics care, to “price in” acute shortages and, over time, make strides to re-balance supply and demand. Regulatory bodies typically refer to network adequacy as a measure of whether the size of a network (i.e., providers, hospitals, specialists, etc.) is adequate to ensure reasonable time to care and coverage for members. Though this system can be flawed – with research findings suggesting that measures are not always accurate and likewise are loosely enforced[23], a tighter incorporation of state Medicaid-led network adequacy measures in Obstetrics could have the potential to rebalance supply and demand in at least some of women’s healthcare.

To avoid reporting of adequacy metrics without action, state Medicaid programs might:

- Define baseline adequacy metrics, for example 1 Obstetrician per 1,000 women of reproductive age within a 30-minute drive.

- Measure networks against this standard annually

- Adjust reimbursement proportionately to any shortages using a reimbursement factor – requiring a plan to increase reimbursement by the % they fall short of their state’s adequacy formula, until such time that provider participation meets the adequacy standard. Though this may feel punitive to payors initially, there should be rebalancing over time as payors see cost savings during the pregnancy episode (within payors’ 1-3 year ROI focus window) as more sites of care deliver better care for women.

This might look like Adjusted Payment = Base Payment x (1 + Adequacy Gap %), to be re-evaluated on an annual basis as adequacy metrics are re-collected.

By strategically raising reimbursement only where it addresses access gaps, like Obstetrics in underserved areas, Medicaid can target its limited funds efficiently rather than broadly inflating payments across all specialty services.

Of course, Obstetrics services are primarily reimbursed through global maternity care codes, which have remained largely unchanged for decades. These codes do not adequately compensate providers for additional patient support during pregnancy and the postpartum period, nor for the administrative work required to deliver such care. That said, implementing an adequacy-gap adjustment to global obstetrics codes should still represent an important first step in addressing the longstanding underpayment in obstetrics, a factor that has contributed to the closure of care sites and reduced access to maternal health services nationwide.

Finally, it is worth revisiting years of debate surrounding the existence of the RUC itself, with many pointing most recently to implications from the Supreme Court’s decision regarding the USPSTF, issued on June 27, 2025, affirmed that its members, as “inferior officers,” do not require Senate confirmation, upholding the ACA’s preventive services mandate. The RUC, by contrast, is a private committee convened by the AMA, with CMS retaining final authority over recommendation adoption. Because the RUC itself is not a federal body exercising delegated regulatory power, it is technically not directly analogous to the USPSTF under the Court’s reasoning. Nonetheless, the decision highlights broader concerns about transparency, accountability, and the influence of non-governmental bodies in shaping reimbursement policy, especially given the reality that CMS broadly adopts the RUC’s recommendations each year.

Foregoing a broad overhaul of the RUC given the massive complexity and likely infeasibility of any such efforts in the near to medium term, we might nonetheless pursue more scoped RUC-focused reform that could have wide-ranging positive effects for Obstetrics and Gynecologic care:

- As mentioned, introduce separate representation for Obstetrics and Gynecology (specifically gynecologic surgery) in the RUC

- Given novel services get higher reimbursements than more established services (and procedures more than E&M services), create a one-time true up by CMS that would outstrip the RUC’s decades of undervaluing Obstetrics and Gynecology care

Collective, policy-oriented action has the promise to positively affect the business of OB-GYN care. In doing so, we can begin to right-size supply and demand—and build a future where OB-GYN care is sustainable for providers and more accessible for patients.

References

[1] Medicus Healthcare Solutions. Insights into the OB/GYN shortage: Understanding the supply and demand gap. Available from: https://medicushcs.com/resources/insights-into-the-ob/gyn-shortage-understanding-the-supply-and-demand-gap

[2] U.S. Department of Health and Human Services, Health Resources and Services Administration, Bureau of Health Workforce. Projections of the supply and demand for women’s health service providers: 2018–2030. Rockville, MD: Health Resources and Services Administration; 2020. Available from: https://bhw.hrsa.gov/sites/default/files/bureau-health-workforce/data-research/projections-supply-demand-2018-2030.pdf.

[3] Association of American Medical Colleges. Labor pains: OB-GYN shortage. Association of American Medical Colleges News. Available from: https://www.aamc.org/news/labor-pains-ob-gyn-shortage.

[4] Healthgrades. OB-GYN appointment wait times vary in 15 metro markets. Available from: https://resources.healthgrades.com/pro/ob-gyn-appointment-wait-times-vary-in-15-metro-markets.

[5] American Medical Association. Development of the Resource-Based Relative Value Scale. Chicago, IL: American Medical Association; [date unknown]. Available from: https://www.ama-assn.org/system/files/development-of-the-resource-based-relative-value-scale.pdf

[6] American Medical Association. Composition of the RVS Update Committee (RUC). Chicago, IL: American Medical Association; Updated July 8, 2025. Available from: https://www.ama-assn.org/about/rvs-update-committee-ruc/composition-rvs-update-committee-ruc

[7] Hsiao WC, Braun P, Yntema D, Becker ER. Estimating physicians’ work for a resource-based relative-value scale. The New England Journal of Medicine. 1988 Sep 1;319(13):835-841. doi:10.1056/NEJM198809293191305. Available from: https://www.nejm.org/doi/full/10.1056/nejm198809293191305

[8] Proudfoot ML. A critique of the practice-expense values of the resource-based relative value scale. Journal of Family Practice. 1993 Jul;37(1):57-67. PMID: 8345341. Available from: https://pubmed.ncbi.nlm.nih.gov/8345341/#:~:text=Abstract,zero%20by%20the%20year%202001.

[9] The evaluation of payment for obstetric and gynecology services. Obstetrics and Gynecology. 2024 Feb;143(2):[page numbers]. https://journals-lww-com.pitt.idm.oclc.org/greenjournal/fulltext/2024/02000/the_evaluation_of_payment_for_obstetric_and.27.aspx

[10] Polan RM, Barber EL. Reimbursement for female-specific compared with male-specific procedures over time. Obstetrics and Gynecology. 2021 Dec;138(6):878-883. doi:10.1097/AOG.0000000000004599. PMCID: PMC8602770. PMID: 34736273.

https://pmc.ncbi.nlm.nih.gov/articles/PMC8602770/#R2

[11] Benoit MF, Ma JF, Upperman BA. Comparison of 2015 Medicare relative value units for gender-specific procedures: Gynecologic and gynecologic-oncologic versus urologic CPT coding. Has time healed gender-worth? Gynecol Oncol 2017;144(2):336–342. DOI: 10.1016/j.ygyno.2016.12.006. [DOI] [PubMed] [Google Scholar], Watson KL, King LP. Double Discrimination, the Pay Gap in Gynecologic Surgery, and Its Association With Quality of Care. Obstet Gynecol 2021;137(4):657–661. DOI: 10.1097/AOG.0000000000004309. [DOI] [PubMed] [Google Scholar], Goff BA, Muntz HG, Cain JM. Comparison of 1997 Medicare relative value units for gender-specific procedures: is Adam still worth more than Eve? Gynecol Oncol 1997;66(2):313–9. DOI: 10.1006/gyno.1997.4775. [DOI] [PubMed] [Google Scholar]

[12] Penn M, Colley D, King LP, Fitzgerald JJ. Price and Prejudice: Reimbursement of surgical care on male vs. female anatomies. Accepted by Journal of Women’s Health, 2024.

[13] American Medical Association. Medicare physician payment adequacy: Budget neutrality. Chicago, IL: American Medical Association; 2024. Available from: https://www.ama-assn.org/system/files/medicare-basics-budget-neutrality.pdf

[14] U.S. Department of Health and Human Services, Health Resources and Services Administration, National Center for Health Workforce Analysis. Projections of Supply and Demand for Women’s Health Service Providers: 2018-2030. Rockville, MD: Health Resources and Services Administration; March 2021. Available from: https://bhw.hrsa.gov/sites/default/files/bureau-health-workforce/data-research/projections-supply-demand-2018-2030.pdf

[15] American Medical Association. Guardado JR. Medical Liability Claim Frequency Among U.S. Physicians. Chicago, IL: American Medical Association; April 2023. Policy Research Perspectives Report 2023-3. Available from: https://www.ama-assn.org/system/files/policy-research-perspective-medical-liability-claim-frequency.pdf

[16] Surana K, Presser L, Suozzo A. Under Texas’ Abortion Ban, More Women Nearly Bled to Death During Miscarriage. ProPublica. Published July 1, 2025. Available from: https://www.propublica.org/article/texas-abortion-ban-miscarriage-blood-transfusions

[17] Schloemann M. OB/GYN Medical Malpractice Insurance. MEDPLI Insurance Services; 2024 Feb 20. Available from: https://medpli.com/specialties/obgyn-medical-malpractice-insurance/

[18] Pelley E, Carnes M. When a Specialty Becomes “Women’s Work”: Trends in and Implications of Specialty Gender Segregation in Medicine. Academic Medicine. 2020 Oct;95(10):1499-1506. PMID: 32590470. Available from: https://pmc.ncbi.nlm.nih.gov/articles/PMC7541620/

[19] Stoneburner A, Lucas R, Fontenot J, Brigance C, Jones E, DeMaria AL. Nowhere to Go: Maternity Care Deserts Across the US (Report No. 4). March of Dimes; 2024. Available from: https://www.marchofdimes.org/sites/default/files/2024-09/2024_MoD_MCD_Report.pdf

[20] March of Dimes. Nowhere to Go: Maternity Care Deserts Across the US, 2024 Report. Arlington, VA: March of Dimes; 2024. Available from: https://www.marchofdimes.org/maternity-care-deserts-report

[21] Silicon Valley Bank. Innovation in Women’s Health Report. Santa Clara, CA: Silicon Valley Bank; 2025. Available from: https://www.svb.com/trends-insights/reports/womens-health-report/

[22] Silicon Valley Bank. Venture Capital Investment in Women’s Health Startups Reaching Record Highs; Silicon Valley Bank Releases Report. San Francisco, CA: Silicon Valley Bank; April 2, 2025. Available from: https://www.prnewswire.com/news-releases/venture-capital-investment-in-womens-health-startups-reaching-record-highs-silicon-valley-bank-releases-report-302417682.html

[23] Hinton E, Raphael J. Medicaid managed care network adequacy and access: current standards and proposed changes. KFF. Published June 15, 2023. Available from: https://www.kff.org/medicaid/issue-brief/medicaid-managed-care-network-adequacy-access-current-standards-proposed-changes/