Word from the Editors

On behalf of the editorial team (Regina Herzlinger, Kevin Schulman, Lawrence Van Horn, and myself), I am delighted to welcome you to the current issue of HMPI. We are proud to publish another strong set of articles that help advance HMPI’s vision: We draw from the research and experience of scholars and practicing leaders to provide insights for public and private health sector organizations around the world. This issue kicks off with a set of articles about a question that has huge topical importance: drug prices in the U.S. and elsewhere. This question never lurks far below the surface of political and industry discourse and the current U.S. administration is considering multiple initiatives that would rein in what it believes are excessive prices. The articles in this issue outline the nature of pharmaceutical markets, discuss alternative pricing systems, and consider how moral hazard that arises due to third party payment may contribute to escalating drug prices. The challenge here, of course, is to find a viable balance of cost-effectiveness with continued development of innovative medicines that support health and healthcare in the U.S. and globally. Together, the articles provide a thoughtful base for considering mechanisms that will help find and maintain that balance.

The issue also features strong new research. Karoline Mortensen, Tianyan Hu, Aleeza Vitale, and Hanns Kuttner address the question of whether healthcare providers offer the same services to Medicaid and private patients. Rachel Hadler, Julia Lynch, Julia Berenson, and Lee Fleisher report on a study of how willing patients are to receive services from nurse practitioners rather than physicians, and whether any preference varies by patients’ political affiliations. Gregory Shea, Jeffrey Kaplan, and Stephen Klasko report a study on the impact of leadership development programs for physicians and non-physicians in academic health centers.

We also draw extensively on the experience of thoughtful leaders with an outstanding set of perspectives articles. Mark Simon discusses how obstetrics hospitalists can help reduce perinatal adverse events. Lilac Nachum outlines how the balance between global and local is transforming the scope of opportunities and raising challenges for healthcare professionals and institutions. Steven Ullmann and Richard Westland report on a recent conference that identified issues that are top of mind for leaders in the U.S. healthcare and life sciences sector.

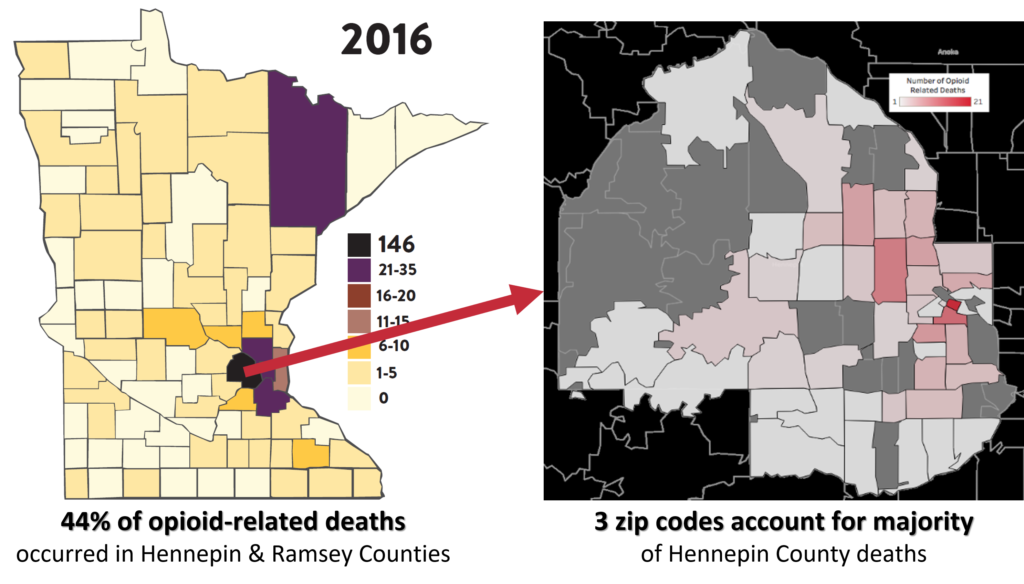

In addition, we are proud to publish the winning entry from BAHM’s 2018 case competition. Elisha Friesema, Stephen Palmquist, and Prachi Bawaskar of the University of Minnesota identify ways of using contagion models from public health to help address the current opioid crisis.

As a final note, we will mention Kristiana Raube’s graduation from the HMPI editorial team. Kristi has taken up the role of country director of the Peace Corps in Liberia. We deeply grateful for Kristi’s leadership in relaunching HMPI. And we are proud of her new leadership in Liberia.

The authors of the articles that we publish in HMPI are committed to improving health systems around the world. We welcome your comments about the articles – please send your comments to us at info@hmpi.org. We also welcome discussion on the BAHM Forum on LinkedIn [https://www.linkedin.com/groups/7042389].

We welcome ideas for potential articles. If you have an idea that you would like to explore for HMPI, please send an outline of your article to our editorial team (info@hmpi.org).

Will Mitchell

Professor of Strategic Management

Anthony S. Fell Chair in New Technologies and Commercialization

Rotman School of Management, University of Toronto

Pharma Prices Are Not Too High (Usually)

Will Mitchell, Anthony S. Fell Chair in New Technologies and Commercialization, Rotman School of Management, University of Toronto

Contact: Will Mitchell, william.mitchell@Rotman.Utoronto.Ca

Abstract

What is the message?

Although drug pricing is highly contentious around the world, with frequent claims of overcharging, average profitability in the pharmaceutical industry is not excessive. Companies need to achieve prices above total average costs if they are to cover the fixed costs of successful and failed development efforts. The most efficient way to accomplish the dual goal of incenting ongoing innovation while also achieving cost effectiveness and broad-based access is to price drugs at different prices in different markets, based on some combination of ability and willingness to pay.

What is the evidence?

Assessment and evaluation of current bio-pharmaceutical industry data, trends, and strategies.

Disclosure: Some of the academic health management programs that I have taught in and several of my research projects have received programmatic support from life sciences companies. This article received no financial or editorial support. All information in the article is based on public sources.

Submitted: October 1, 2018; accepted after review: October 31, 2018.

Cite as: Will Mitchell. 2018. Pharma Prices Are Not Too High (Usually). Health Management Policy and Innovation, Volume 3, Issue 2.

Drug pricing has been controversial in the U.S. and elsewhere essentially as long as drugs have been sold. In 1959-1960, the Kefauver Drug Hearings conducted by the U.S. Senate Subcommittee on Antitrust and Monopoly concluded that pharmaceutical firms did not merit the prices they were charging; [1] moreover, as William Comanor put it in 1966, “the committee charged that little of social value came from industry laboratories”. [2] Scrolling forward to the present, in the past decade or so, prices have escalated far higher, particularly as the biological revolution has taken hold, with some drugs now having list prices in the tens and even hundreds of thousands of dollars.

With increased drug prices has come scrutiny and debate. Perhaps the only thing that the three highest profile candidates in the 2016 U.S. Presidential primaries and election – Donald J. Trump, Hillary Rodham Clinton, and Bernard Sanders – agreed on was that drug prices are far too high. Article after article in the press and media in the U.S. and other countries, as well as highly publicized Congressional hearings, have reported claims of high prices and massive price increases, sometimes targeting individual executives as responsible for price gouging. The current U.S. administration has announced an ongoing sequence of potential initiatives directed at what it believes are excessive prices. [3] And in the 2018 Gallup poll of industry reputation, the pharmaceutical industry finished 29th of 30, with a net negative rating of 23% [30% positive; 53% negative], slightly ahead of only the U.S. federal government. [4] Clearly, drug prices must be too high.

Yet what would it mean for prices to be “too high”? The simplest conceptual case would be that value received by patients and other stakeholders in the healthcare system does not justify the prices charged by pharmaceutical companies and intermediaries such as distributors, presumably because the companies have market power that allows them to price above marginal cost. Yet, as I will argue in this article, a close look at relevant data does not support this conclusion.

Instead, thoughtful assessment suggests that average profits in the pharmaceutical industry are largely in line with the companies’ needs to support ongoing development and commercialization of new drugs and related services. Although some individual cases may be questionable, the overall pattern is one of an industry that typically acts responsibly in supporting necessary business activities while seeking to provide value for patients.

I will start with the assumption that recent advances in drug therapies are making important contributions to healthcare and human health. While there are credible debates about marginal value and concerns about side effects of some drugs and, especially, which patients they might be suited to, there are undoubted major contributions in areas ranging from multiple types of cancer, to Hepatitis C, to a broad set of immunological diseases, to ophthalmic needs, to HIV/AIDS, and a host of other conditions. [5] Moreover, the companies that market these drugs also are increasingly providing a range of support such as infusion services, patient and provider education, patient financial support, nutrition and life style counselling, pay for performance contracts, and other services that provide far more encompassing value than simply a core pill or injection.

Some of these advances of drugs and complementary services serve tens of thousands of people. Others serve only a few individuals who suffer from orphan diseases. Again, while it is entirely reasonable to question whether a particular therapy suits an individual patient in a given context, the overall impact is contributing to solving real human medical needs

Rather than a single price, drugs have multiple prices

Of course, improved health by itself is not enough to end an argument about the industry. There needs to be a corresponding judgement about cost effectiveness [6], as reflected in the price that drug companies receive from the myriad types of payers. This is where the controversy arises. Yet payers, particularly third party payers such as pharmaceutical benefit management companies (PBMs) with substantial market power of their own, have substantial ability to negotiate discounts and rebates, manage formularies, and shape whether drugs achieve market access. [7]

In practice, actual prices to most payers typically are far below list prices that show up in public reports such as Average Wholesale Price (AWP), which one of my colleagues informally likes to refer to as “Ain’t What’s Paid”. Indeed, for almost all drugs, there is no one price – instead, there are multiple prices, sometimes even to the same payer, based on negotiations, public mandates, pressure from patients and patient advocates, and market conditions.

It is not my intent here to argue that any one price to any one payer is “too high” or “too low”. It is the job of any payer to negotiate a price that meets its own definition of value. And there may well be appropriate opportunities to help some payers increase their negotiating strength and sophistication, and so help the healthcare system meet the goals of cost effectiveness and broad access.

Rather, my aim is to argue that the overall revenue that drug companies receive from payers aligns with the health system’s complementary goals of creating incentives for ongoing innovation and for providing as broad access as possible to appropriate health services. Several metrics and practical conditions of the industry underlie this conclusion. In the next sections, I will discuss profitability, the need for average prices of pharmaceuticals to exceed variable costs, and the increasingly short time window for companies to recoup fixed costs of developing and bringing drugs to market before they face generic competition.

Average profitability grew through the early 2000s and then declined

Using companies’ financial statements, I have collected data on more than 70 major pharmaceutical firms that have sold branded pharmaceuticals, including long established companies and new biological entrants based in Western Europe, North America, and Japan, with data for most firms going back into the 1970s or earlier. The most complete period, 1990 to 2017, includes 33 to 50 firms per year, with the numbers varying due to consolidation. Where appropriate, I also draw data on the more than 500 public pharmaceutical and biological firms listed in the Compustat data base. This section and the discussion of costs that follow will be a bit numbers heavy, because it is necessary to use real data to provide an accurate picture of the industry and relevant trends.

The simple story of pharma profitability is that it grew and then declined. In the 1980s and early 1990s, bio-pharma firms’ median profitability based on return on sales (ROS) was about 7% to 11%, a comfortable but not particularly high rate of return. During the 2000s, with the introduction of new generations of large market drugs, median ROS grew to a maximum of 17% in 2009.

Then, between 2010 and 2017, list prices of many high profile new drugs, particularly newly-approved biologicals, increased substantially. One might expect corporate profits to have grown even higher in the past decade.

However, rather than continuing to increase, median return on sales in the industry has declined: falling to 13% to 14% in each year from 2014 to 2017 (the trends are similar if we base profitability on return on assets). Within the average, there is substantial variance. In 2017, for instance, the profitability of 33 companies with a median ROS of 13% ranged from a high of 41% (reflecting gains from the sale of a major business unit) to a low of –9% (reflecting ongoing losses at a biological specialist). In 2016, with median ROS of 14%, the maximum and minimum ranged from 45% (a win from a blockbuster biological) to –56% (the same financially struggling biological specialist as in 2017).

While some firms in some years have achieved particularly high profitability, occasionally even with ROS of 40% or higher – 1.5% of the cases among 1,193 years of observations for 61 unique firms in my data from 1990 to 2017 exceed 40% ROS; 5% exceed 30% – such cases typically last at most for a few years and fall again as competing products enter the market. Hence, even as list prices have increased, average profits in the industry have fallen.

Overall, the bio-pharma industry is now comfortably profitable on average, but far from levels that suggest massive systemic price-gouging. Indeed, major ongoing price reductions on the scale that some critics appear to believe appropriate would quickly lead to untenable financial levels for most or all firms.

Consider the simple math: if the median firm with 13% ROS in 2017 was forced to cut its net prices by 10% with no other changes to its business model, it would barely clear break even. And most of the half of its competitors with ROS below the median value would fall to break even or below. The arithmetic becomes a bit more complicated if the price cut only applied to U.S. sales, which typically mark well over 40% of a U.S. based company’s revenue (and often much higher) and lesser but still substantial proportions for European and Japanese pharma firms, but the financial impact would quickly be unsustainable. Yet a 10% price cut is well below what the debate would suggest is needed.

Cross-industry comparisons of multiple profitability metrics (e.g., return on sales, assets, capital, and equity) based on reports from the industry analyst firm CapitalIQ show that the pharmaceutical and biological industry categories tend to be somewhat more profitable on average than the S&P 500 list of the largest public firms, commonly at about the level of technology and computer hardware companies, but again well within a range of normal profitability. Why, then, have bio-pharma profits declined as list prices – and controversy about prices –have increased?

The costs of doing business have increased

I will highlight four reasons for declining profitability during the past decade: discounts, production costs, R&D expenses, and marketing expenditures. First, part of the cause for the decline in average profitability is the issue I noted earlier: list prices are largely meaningless. During the past decade, third-party payers in the U.S. have become increasingly aggressive about demanding discounts in return for agreeing to include drugs on their formularies of drugs approved for their covered lives. Particularly as competitor products enter a therapeutic class, negotiated discounts commonly increase and net prices fall.

While most discounts are confidential, reports from Kaiser Permanente, investigative journalists, and others suggest that rebates can reach 25% to 50% or more of list price. Hence, while a company with a first-to-market blockbuster may enjoy a few years of high profitability, competition and reactions by payers tend to bring it back down.

Second, many of the newer biological drugs are more expensive to produce than earlier generations of small-cell pharmaceuticals. Median “cost of goods sold” (COGS), i.e., production costs of the drugs, of two dozen major firms I am tracking has grown from about 21% in 2000 to 25% in 2017. While not a huge increase, the extra costs have been enough to affect profits.

Third, the costs of developing and obtaining new drugs have increased due to increasing need for multi-source development activities. It simply is not possible for a single company to possess all the skills needed to bring a full portfolio of drugs to market by relying solely on internal development. Instead, bio-pharma firms now employ a sophisticated set of build, borrow, and buy strategies to source new drugs, including a complex mix of internal R&D, alliances, and acquisitions.

The extent of both acquisitions and alliances has grown strikingly according to figures reported by data bases such as ReCap, Cortellis, CapitalIQ, and SDC Platinum. The annual number of M&A deals has grown from 150 to 200 in the late 1990s, to more than 500 in 2017. Some M&A deal values reach billions of dollars: Cortellis reports more than $250 billion in global bio-pharma acquisition value in each of 2016 and 2017.

Inter-firm alliances in the sector also have become increasingly common. In 1990, fewer than 350 alliances were reported in industry data bases. In 2017, depending on the data source, the reported number had grown to somewhere between 2,500 and 4,000 partnerships. While alliances tend to have lower deal value than acquisitions, annual expenditures now total multiple billions of dollars.

Internal R&D costs, meanwhile, rather than decline as acquisitions and alliances have increased, have also grown. Annual R&D expenditures by 22 major bio-pharma firms in 2000 reached about $32 billion; in 2017, the top 17 bio-pharma companies spent about $73 billion. Across the full set of publically traded bio-pharma firms reported by Compustat, R&D expenditures in 2000 and 2014 grew from $51 billion to $118 billion. In addition to sheer magnitude, R&D has also grown as a percentage of sales: among the leading firms, the average ratio grew from 15% in 2000 to 18% in 2018.

Fourth, selling, general, and administration (SG&A) expenditures also have grown, though at a slower rate than R&D. SG&A is an indicator of marketing and other commercialization activities, including the costs of patient support that are now important parts of the suite of services that complement a core drug. Compustat data for public bio-pharma firms report SG&A growth from about $150 billion in 2000 to $280 billion in 2014.

Despite the growth in magnitude, average SG&A as a percentage of sales has remained stable or even fallen; among the top 30 to 40 firms, the ratio fell from 35% in 2000 to 28% in 2017. The reduction in the marketing cost ratio reflects the shift in strategy during the period, from emphasizing large market drugs such as cardiovascular statins and gastro-intestinal proton pump inhibitors, which require large sales forces, to placing greater emphasis on products such as immuno-oncology drugs prescribed by specialist health care providers, which require more targeted commercial support. At the same time, though, the newer drugs have required substantial patient support as well as market access expenditures in negotiations with third-party payers, which limits the ability to undertake further reductions in expenditure.

The core point here is that multiple aspects of development and commercialization costs have grown more quickly than revenue during the past decade or so, despite the frequent claims of excessive price increases. The expenditures reflect the real costs of doing business in the bio-pharma sector: obtaining and creating new drugs, conducting trials, manufacturing the drugs, gaining market access, and supporting them in the market. Currently, the industry is not under a threat of failure but also is not at any obvious level of excessive profitability that would support extensive price cuts. While individual firms may enjoy very high profits for a few years, they typically return to earth; the overall profile is reasonable. In parallel, firms may suffer low or even negative profits in some years – 14% of the annual observations for the major firms in my data from 1990-2017 report losses – but typically return to reasonable levels, or are purchased by competitors who can use their resources more effectively.

Fixed costs are high, with a substantial gap between variable costs and total average costs

Now let’s leave the deep dive into data and consider the nature of costs in the industry. Bio-pharma is marked by high fixed costs in R&D, whether done internally or paid for via alliances and acquisitions. Successful projects typically require many years and many millions of dollars in lab work, clinical trials, and regulatory expenses, whether initially sourced internally or externally. And many projects fail – that is the very nature of experimentation – sometimes early in the development cycle after a few million dollars but occasionally reaching into the hundreds of millions or more if a drug proceeds to large scale Phase 3 trials before failing.

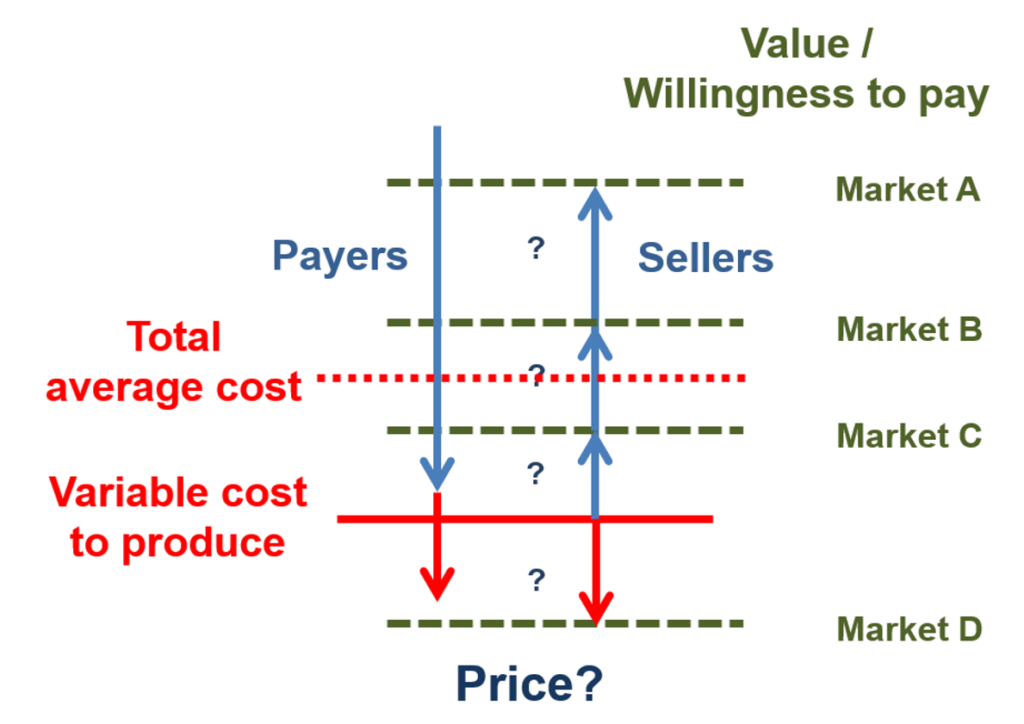

Figure 1 builds on this point. Development costs, including the costs of failures, are fixed costs. As such, they do not show up in the average variable costs required to produce and support a drug and its associated services in the market. The high relevance of fixed costs creates a substantial gap between “Variable cost to produce” and “Total average cost”, as the horizontal red lines in the figure depict.

Figure 1. Bio-pharma value, costs, and prices

The gap between variable costs and average total costs introduces a major issue in bio-pharma price negotiations. The goal of a pharmaceutical firms’ negotiator is to gain a price as close as possible to a buyer’s value ceiling (the horizontal green dashes in the figure). Yet few buyers will simply pay for the full value they receive from any product – including products that produce health value – if they can negotiate a lower price.

Instead, the goal of any payer is to negotiate price down as close as possible to its estimate of the seller’s average variable cost. That is the minimum price below which a producer cannot cover its operating expenses. And, if pushed to the limit, the variable cost floor is the price that a seller will settle for: this rate at least covers the costs of producing and selling the drug. Where the price ends – up near the value ceiling or down on the variable cost floor – depends on the comparative bargaining power and negotiation skill of the buyer and seller.

This is a challenging negotiating calculus. All payers in the health sector face real pressure on their budgets, with increased prices for pharmaceutical products creating part of those pressures. In the U.S., prescription pharmaceuticals accounted for almost $325 billion in 2015, about 10.1% of national health expenditures (up from 8.8% in 2000), behind the hospital (32%) and physician/clinical (20%) shares. [8] In Canada, drug expenditures reached about 16.2% of national health expenditures in 2016, behind only hospitals (29%), up slightly from 15.4% in 2000. [9] Hence, even though a payer may recognize and even embrace the high health value ceiling of a pharma product, it needs to push as hard as possible to bring prices down toward the variable cost floor.

The individual buyer’s goal to push prices to the floor in turn creates the rub for the seller. If every payer successfully negotiated a price that just met a drug’s average variable cost, then the company producing the drug would fail because it was not covering its fixed costs of development. Instead, a bio-pharma firm requires some degree of negotiating power to charge at least some buyers prices that exceed the minimum market clearing price, shifting up toward the value ceiling.

Indeed, this is one of the purposes of the patent system: to provide a successful innovator with a period of exclusivity in which it can recover the costs of creating the innovation. Then, once a patent ends or, equally powerfully, once a product with similar therapeutic value enters the market, competition will drive prices down toward marginal costs. This balance – of incentive to innovate and competition to bring on subsequent price pressure – is central to patent policy and law.

Now let’s use Figure 1 to make things a bit more complicated, while introducing a necessary part of pharmaceutical pricing strategy. The bio-pharma market, like almost all markets, has multiple segments, with different customers who have differing ability and willingness to pay for a product. In Figure 1, these segments are depicted as Markets A, B, C, and D. For a pharmaceutical company, the goal is to identify the combination of value and ability to pay for each segment and, ideally, settle on prices that come close to that value ceiling for each market, while surpassing variable costs. Such price discrimination strategies are profit maximizing.

Market segmentation introduces pricing variation across and within countries. For instance, prices are commonly lower in lower income countries such as Greece and Spain, versus higher prices in higher income countries such as Germany and the U.S. Even within countries, different payers commonly have different ability to pay. In the U.S., for example, the state-based Medicaid systems are mandated to receive the lowest price negotiated by any other actor, while other payers such as employment-based PBMs commonly have greater latitude and financial resources.

In such cases of multiple market segments with different ability to pay, a pharma company’s dominant strategy is to set different pricing points for each segment. To be sustainable, the strategy needs to result in some prices being high enough above the variable cost floor, in aggregate across the company’s portfolio of products, to cover the gap between that floor and total average costs.

Market D in Figure 1, where buyers are not able or willing to pay enough to cover even the variable costs of production, introduces a further complication. In most industries, sellers would ignore this segment. Yet in healthcare markets, most people – including most people who work in pharmaceutical companies – feel a responsibility to reach as many patients as possible, including those who cannot pay enough to cover operating costs. While no public or private actor can afford infinite below cost contributions, there is real need and desire to provide access to as much of the population as possible. For pharma companies, this is part of the basis of patient assistance programs, which provide subsidized or free drugs and services when people in market D lack insurance or personal resources. In turn, though, such below cost strategies place even more pressure to move well above the variable cost floor when negotiating with buyers in market segments A, B, and C.

Quite simply, “too much” pressure to drive prices down will lead to two negative consequences. In the short term, the pressure will drive out a company’s ability to provide cross-subsidized services below the variable cost floor. In the longer term, the pressure will drive innovative firms out of the market because they cannot cover the gap between variable and total costs.

Time windows before competitors enter have become shorter

Now consider time windows for pharmaceutical companies to earn high prices, even after discounts. The key issue here is penetration of the market by generic drugs and “biosimilars” of biologics. Before the 1984 Hatch-Waxman legislation facilitated entry of generic competitors when drugs came off patent, generic drugs made up about 20% of prescriptions in the U.S. Generic penetration grew to about 40% in 2000. Today, as generic and biosimilar competition has become much more active, and as payers respond to pricing pressure by mandating generics on formularies whenever possible, the generic prescription rate in the U.S. is about 90%. Most traditional developed markets also are at substantial, if somewhat lower, levels; Canada, for instance, has a generic prescription rate of about 70%.

Moreover, under the rules of Hatch-Waxman and similar policies around the world, generic approvals have grown exponentially. In 1984, the U.S. FDA reported 66 approvals; in 2017, there were 847 generic approvals. [10] Generic competitors are commonly lined up to enter the market immediately when a drug goes off patent, particularly if the drug had achieved a substantial market size.

Once generic competitors enter, prices fall, sometimes drastically. Prices for traditional large market drugs with multiple generic competitors commonly face price reductions of as much as 90%. Price reductions for the specialized biologicals that have begun to go off patent and face biosimilar competition have been less striking, because so far there are fewer competitors. Nonetheless, the reductions are substantial, with discounting in the range of 35% commonly being reported.

Once generic competition becomes active, prices move, often rapidly, toward the variable cost floor in Figure 1. From the point of view of payers, this is a good outcome. And, again, this is one of the goals of the patent system: provide a period of exclusivity as an incentive to innovate, then open the doors to competition to create incentives to innovate again as well as providing cost effectiveness in the market.

From the point of view of a bio-pharma innovator, though, this increasingly striking combination of early generic entry and strong price reductions means that there are far fewer years than there once were to earn the profits needed to cover the gap between variable and fixed costs. If the firm is going to survive, it needs active strategies to deal with the shorter window.

Time window strategies have had two major components, both of which we have noted earlier. First, companies are increasingly emphasizing specialty drugs. This is partly a feature of the biological revolution, which has created opportunities for major contributions to health for targeted medical needs. In addition, drugs for specialty market segments such as oncology and immunology, whether based on biological or older science, typically face lower rates of post-patent generic competition, both because only a few firms currently have the skills needed to compete effectively and because specialty prescribers and patients are often reluctant to switch away from drugs that they have come to understand and rely on. Hence, even after patents expire, specialty drugs commonly achieve prices above the variable cost floor, sometimes for multiple years.

Second, firms have increased the initial prices they charge during the shorter protected window, in order to generate income as quickly as possible before facing generic or biosimilar competition. Thus, the policy changes that have encouraged price competition from generics – as desirable as these policies undoubtedly are for payers, patients, and the health system – have also created strong pressures to increase prices that policy makers are now complaining about. The quid of competition and long term price reductions has induced a pro quo of initial price increases.

Where does this leave us?

The key question is whether healthcare systems in countries such as the U.S. are now reasonably close to achieving a balance of innovation and cost effectiveness or, as some voices implicitly claim, can we continue to maintain incentives to innovate while drastically bringing down pre-generic prices? My interpretation of the data and observation of strategies and incentives is that we are fortunate to have an actively innovative bio-pharma sector, made up of a complex and dynamic mix of established firms, new ventures, academic and government scientists, complementary firms, and regulatory bodies, paralleled by a critically important set of generic manufacturers (some of which are the same companies) that help provide discipline in the system. This quasi-market is far from fully efficient – no market is – but it has evolved to a point of generating and commercializing new bio-pharmaceutical products and supporting services at a rate that is higher than at any point in the history of the industry.

Consider recent innovation. Just as approval of generics is increasing, so is approval of new drugs. In 2017, the U.S. FDA reported granting 54 new approvals, including 21 biologicals. This was the highest rate ever (other than a 1996 clean out of the approval pipeline), up from 29 (2 biologicals) in 2000. The companies that received the approvals included a wide mix of established pharmaceutical firms from Western Europe, Japan, and the U.S., plus an even wider mix of new ventures and smaller specialty companies.

Now consider market entry. Innovator companies commonly apply for FDA approval and introduce their drugs to the U.S. market before entering other countries. The prices available in the U.S. are not as much higher than those in other traditional developed markets as reported list prices would suggest, but on average are somewhat higher, due in large part to the multiple segments available for price discrimination. In turn, profitability in the U.S. is higher: the few firms that report geographic profit margins commonly recognize operating profits as a percentage of sales that are 15% to 25% higher in the U.S than in Europe. Higher prices and profits typically lead to faster entry, earlier access to novel treatments, and ultimately, earlier access to lower-priced generics once the innovators’ patents expire.

It is important to recognize that there are outliers in the system. Some companies earn very high profits, though typically for only a few years. In part, the hope of such profits can be viewed as a lottery that incents entry to the industry. Indeed, there are far more companies with very negative profitability than very positive results – the median return on sales of all bio-pharma companies in the Compustat data base (now more than 500 firms) has been negative each year since 1989. The lure of a payoff is a necessary complement to the uncertainties of experimentation.

There are also outliers in pricing strategy that on the face, and likely even the depths, of it do appear unreasonable. Massive increases in prices of sole-source generic drugs that can be maintained until competitors gain approval and enter, which typically takes several years, stick in many craws. But it is important to recognize that these are outliers and not to develop general policies targeted at extreme cases.

A key point here is that it is equally important to recognize that lower prices typically lead to later entry and sometimes no entry at all. Introduction rates to lower priced southern European markets, for instance, are substantially lower than in North America or much of northern Europe. Simply forcing prices to a lower level in any given country, whether the U.S. or elsewhere, would almost certainly lead to reduced entry in that country.

Nonetheless, there is an active policy and health question here, of when higher initial prices in a market – and consequent more active entry – are balanced by greater health benefits. The answer to that question requires engagement of multiple stakeholders in the health system, including payers, prescribers, regulators, bio-pharma companies, and patients. Currently, once a drug has received market approval, payers such as PBMs have become increasingly powerful gate keepers in access, with their role in setting formularies. There is real strength in that role, but there are also opportunities for more effective engagement of the other stakeholders in assessing costs and benefits.

If there is a need for policy initiatives, the goal of integrating insights across the fragmented silos of the healthcare system in the U.S. and elsewhere is far more of a priority than the marginal reductions in prices that could be accomplished without drastically damaging the ability of innovator companies and their generic followers to provide continuing health value. Rather than the current debate about costs, we would be much better served by a debate – and action – about appropriate value.

References

- Daniel C. Morgan, and Samuel E. Allison. 1964. The Kefauver Drug Hearings in Perspective. Southwestern Social Science Quarterly, 45 (1): pp. 59-68. https://news.gallup.com/poll/12748/business-industry-sector-ratings.aspx

- William S. Comanor. 1966. The Drug Industry and Medical Research: The Economics of the Kefauver Committee Investigations, The Journal of Business, 39 (1): pp. 12-18. https://www.jstor.org/stable/2352011?seq=3#metadata_info_tab_contents

- Yasmeen Abutaleb and Michael Erman. 2018. Trump seeks to base Medicare drug prices on lower overseas rates. Health News, October 25. https://www.reuters.com/article/us-usa-trump-drugpricing/trump-seeks-to-base-medicare-drug-prices-on-lower-overseas-rates-idUSKCN1MZ2SF

- https://news.gallup.com/poll/12748/business-industry-sector-ratings.aspx

- As one of many examples of studies of health benefits, see a discussion of health benefits for rheumatoid arthritis see: John J. Cush and Kathryn H. Dao. 2007. Perspectives on Safety vs. Benefits of Biologic Therapies. Medscape Rheumatology. https://www.medscape.org/viewarticle/553515_4

- Robert S. Kaplan, Michael E. Porter, Mark L. Frigo. 2017. Managing Healthcare Costs and Value. Strategic Finance 98 (no. 7): pp. 24–33.

- Cole Werble. 2017. “Health Policy Brief: Pharmacy Benefit Managers,” Health Affairs, September 14, 2017. DOI: 10.1377/hpb20170914.000178

- Centers for Medicare & Medicaid Services, Office of the Actuary, National Health Statistics Group.

- Canadian Institute for Health Information (CIHI): https://apps.cihi.ca/mstrapp/asp/Main.aspx

- Drugs@FDA: http://www.accessdata.fda.gov/scripts/cder/drugsatfda/index.cfm?fuseaction=Reports.NewOriginal_ANDA

Healthcare Leaders Reflect on the Business of Healthcare Today

Steven G. Ullmann, PhD and Richard Westlund, MBA, University of Miami Business School

Contact: Steven G. Ullmann, sullmann@bus.miami.edu

Abstract

What is the message?

What issues are top of mind for leaders in the U.S. healthcare and life sciences sector

What is the evidence?

Discussion among industry, clinical, and policy leaders at the University of Miami’s annual “Business of Health Care” conference on topics ranging from healthcare policy to the opioid epidemic.

Submitted: May 18, 2018; accepted after review: July 20, 2018.

Cite as: Steven G. Ullmann, Richard Westlund. 2018. Reflections by Health Care Leaders on the Business of Health Care. Health Management Policy and Innovation, Volume 3, Issue 2.

The Center for Health Management and Policy at the Miami Business School, University of Miami, recently hosted our seventh annual conference on “The Business of Health Care.” Our objective at each conference is to understand how the different sectors of the health care industry are impacted by changes in government policies, as well as technology, finance, and consumer trends. Most generally, we want to understand how the health care sector is impacting business and society as a whole.

This year’s conference theme, “What’s Next?”, drew more than 700 business executives, health care professionals, and students, including regional, national, and global leaders in their fields. The focus was on how the failed Congressional effort to repeal and replace the Affordable Care Act (ACA) would affect the health care sector, heathcare access, cost, and quality, as well as business in general.

This year’s panel consisted of Pamela Cipriano, President of the American Nurses Association; Joseph Fifer, President and CEO of the Healthcare Financial Management Association; Richard Pollack, President and CEO of the American Hospital Association; Marilyn Tavenner, President and CEO of America’s Health Insurance Plans; and Halee Fisher-Wright, M.D., President and CEO of the Medical Group Management Association. The panel was moderated by Patrick Geraghty, CEO of GuideWell Mutual Holding Company, the parent company of Florida Blue.

Discussion initially focused on healthcare policy developments in Washington, D.C. The consensus was that with the midterm elections looming, little legislative action was expected from Congress. Rather, there have been policy changes from the executive branch through adjustments to regulations and tweaks to the Medicaid system. Two key areas of change were federal approval for health plans that are not totally compliant with the Affordable Care Act, and the movement away from national policy to state policy with respect to Medicaid access and coverage.

Access to private insurance was another point of discussion. High premiums, copays, and deductibles are impacting and implicitly challenging the concept of healthcare as a right in the United States. To address limitations in access to healthcare, the panelists discussed allowing nurses to practice at the highest levels of their education and training. While licensing policies differ from state to state, this could help address the access issue, both financially and geographically.

There was significant discussion concerning the value proposition:

Value= Quality/Cost,

and the movement from volume- to value-based reimbursement. Hospitals are seeing the move from fee-for-service to fee-for-value. Value is being addressed with focus on such aspects as readmissions, non-compliance with reform experiments, and shared-risk CMS programs for physician practices and other provider organizations. However, population management and capitation methodologies are still not widespread. The panelists also examined the many pilot projects associated with the creation of value, such as the 80 payment reform experiments underway in one large healthcare system alone. Further, the Accountable Care Organization trend has had mixed success, although it may be helping to bring some care teams into alignment.

One of the items on panelists’ minds was the opioid epidemic in the United States. It was indicated that the nursing profession is on the front line of pain management. There have been in excess of 50 bills discussed in Congress (though that has narrowed down to one). At the same time that there has been a crackdown on prescription opioids. Indeed panelists indicated that, because of the attention paid to the issue, that there has been a 30-40 percent drop in opioid prescriptions.

It was made clear, however, that there is a role for opioids in the management of pain in both the hospital and home care environments. Unfortunately, now we are in a situation where those who prescribe opioids are “being blamed.” The panelists also noted that while much attention has been paid to the opioid epidemic, issues associated with alcoholism and alcohol-related deaths have not been discussed in depth, although they are also a very serious public health issue.

Returning to the theme of value-based purchasing (Quality/Cost), the panelists quickly came to agreement that an area of significant opportunity was in the management of chronic conditions. Given the aging of Americans, a focus on wellness, patient compliance, care at home, and human contact can all significantly improve quality of life without adding significantly to the cost side of the equation. This is an area where Congress is in need of education as to effective spending especially given the limited federal budget to attain the most effective patient and population health outcomes.

Reflecting the diversity of the panelists – who represented medical group management, nursing, hospital and health care systems, financing of these systems, and providers, as well as the insurance sector – the closing remarks centered on the need for teamwork to improve the quality of medical care and patient outcomes in the U.S. and globally in a cost-effective manner.

First Do No Harm: How an OB Emergency Department Can Help Reduce Perinatal Adverse Events

Mark N. Simon, MD, MMM, CPE, Ob Hospitalist Group

Abstract

What is the message?

Obstetrics is a highly-charged environment. Under the traditional “call model” of hospital obstetrics, siloed care can create an atmosphere ripe for error. Hospitals can reduce adverse events by identifying the factors that lead to gaps in care and implementing better solutions. An examination of claim frequency data suggests an OB hospitalist program centered on early team-based involvement and assessment of the patient is associated with reducing harm from occurring during labor and delivery.

What is the evidence?

Data from Clarity PSO reveals that the second highest rate of harm events (among event types) are perinatal events, with 66 percent involving harm, compared to 24 percent of “no harm.” An analysis by Ascension Health of key risk mitigation strategies identified the use of OB hospitalists at their hospitals as a valuable best practice initiative in driving down the loss, with a 31 percent reduction in serious harm incidents before and after program implementation.

Submitted: July 11, 2018. Accepted after review: July 20, 2018

Cite as: Mark N. Simon. 2018. First Do No Harm: An OB Emergency Department Can Help Reduce Perinatal Adverse Events. Health Management Policy and Innovation, Volume 3, Issue 2.

“Adverse event” is an oddly innocuous and impersonal word when used in context of healthcare delivery.

Technically, “adverse event” describes a clinical incident where unexpected injury/harm is caused by medical management or a complication rather than the underlying disease. But the term “adverse event” removes the incident from its genesis – the root cause of harm – and harm is personal and rarely innocuous.

For the patient, an adverse event can impact safety, health, and well-being, often leaving in its wake anger, sadness, pain, and grief. To a clinician, an adverse event means something, be it major or minor, went wrong with his/her patient care; the thought of possibly playing a role in that error can lead to self-blame, doubt in professional abilities, depression, and burnout. And even a community also bears some of the impact of an adverse even, albeit in a less personal way. Healthcare may be a business, but it also is a service delivered by individuals and respected community institutions. When an adverse event occurs, there is risk that the community will lose trust in a clinician or a beloved institution.

Adverse events also have wide-ranging ramifications and a long shelf-life. For hospital administrators, risk managers, or c-suite executives, an adverse event can make it challenging or impossible to achieve organizational goals, and more likely lead to impacts ranging from reputation damage to exposure and litigation.

Now, add to that powder keg the unique dynamics of a hospital obstetrical unit.

There is the hope and possibility, but not the guarantee, of a happy, healthy outcome for mother and child. This is not only the outcome that is desired by the family, but also an outcome that is assumed by modern society. So when an adverse event occurs, the ripples and repercussions are even more pronounced.

Given these dynamics, there is enhanced potential for processes to break down and rapid response times to lengthen. By its very nature, the unexpected can occur in this setting, and an uneventful delivery can quickly become a life-threatening emergency. In comparison to other medical professions, obstetrics is also anomalous in that not just one life is at stake, but two.

In a perfect world, adverse events would not occur in obstetrics. But healthcare is imperfect; despite best practices, we don’t have the ability to preempt emergencies, the tools to change or reverse the inevitability of disease progression, or the answer to every medical mystery. On top of that, healthcare – like a baby – is delivered by humans. And humans make mistakes.

What if we focused on transforming the Labor & Delivery structure so that mistakes rarely occur?

While adverse events may never be totally eliminated, we can pursue that goal by not just tracking, but by better understanding the data related to adverse events, addressing the factors that lead to gaps in care, and filling those gaps with better systems and solutions. In short: in addition to lowering harm events themselves through obstetrical best practices, we must avoid potential for harm by changing the ecosystem itself.

Healthcare delivery systems can start that process by closely examining Patient Safety Organization (PSO) perinatal practice data to identify opportunities for interventions. In general, “harm events” can be characterized as having no harm (in that a reportable event happened but there was no harm done); mild harm; moderate harm; severe harm; or death. Many hospitals examine their data and classify their events into one of those five categories.

A recent examination of data on harmful events by Clarity PSO, one of the nation’s largest Patient Safety Organizations, reveals that the second highest rate of harm events, within event types, are perinatal events. Given the reasons outlined above, perhaps that is to be expected. But of those, 66% involve harm, compared to 24% of “no harm.” In almost every other category, “no harm” events are about twice as high as “harm events.”

These data suggest that, even in highest risk area of medicine, harm reduction initiatives may not go far enough in getting to the fundamental cause of adverse events. But the data also speak to complexity of OB/GYN care – and the importance of having a team-based approach to collaborate proactively, and to anticipate potential problems that could result in unintended harm.

In a traditional call model, there are numerous factors that may contribute to an environment ripe for error. Those factors include disparity of care, reliance on telephone triage, delays in care, patient miscommunication/dissatisfaction, doctor/midwife practice interruptions, and doctor/midwife stress and fatigue. Many of these factors are exacerbated by the siloed care that occurs in the traditional call model, in which one nurse runs triage for a presenting patient and then communicates, often without the benefit of the full clinical picture, to other stakeholders including the clinician. Both individually and collectively, these factors detract from a culture of safety and harm reduction.

Worse, the traditional call model is based on the “wait….wait…wait…NOW!” system of delivery. Under the watchful eyes of the nursing staff, a woman labors until the decision is made to call her obstetrical clinician, at which point the OB must drop everything – seeing patients in her clinic, having dinner, sleeping – and get to the hospital for the delivery. That potential delay in care is associated with 31 percent of OB claims (22% related to delay in recognizing and treating fetal distress, another 9% with delays in delivery).[1]

The laborist model, in theory, was designed to surmount those challenges. A term first coined in 2003, “laborists” were OB/GYNS who were primarily responsible for the management of laboring women and emergencies in Labor & Delivery. As the model evolved – and terminology changed to “ob/gyn hospitalist” – the American College of Obstetricians and Gynecologists added its stamp of approval, noting in a Committee Opinion that it, “…supports the continued development and study of the obstetric and gynecologic (OB-GYN) hospitalist model as one potential approach to improve patient safety and professional satisfaction across delivery settings. Standardization of medical care has been shown to lead to improved outcomes, and OB-GYN hospitalists can serve as a driving force behind the implementation of these protocols in labor units.”[2]

Since 2003, hospitals have explored differing models with varying degrees of success. Some hospitals use in an in-house model, in which existing staff OBs perform limited OB/GYN hospitalist duties. This can be difficult for these clinicians who are simultaneously caring for their private patients while performing OB/GYN hospitalist duties, making them susceptible to being over-extended. Other hospitals use a physician employment model, in which physicians who may or may not also have a private practice are employed by the hospital to perform a contractual list of OB/GYN hospitalist duties. A third option is the management model, in which hospitals contract with outside companies to recruit and manage OB/GYN hospitalists who provide a wide array of services, implement the program, and oversee its operation.

An aspect included in some of these models that has emerged in recent years is the Obstetrical Emergency Department (OBED). Under an OBED model, all OB patients presenting with an emergency condition are seen by a physician or midwife alongside the obstetrical nurse. Emergent issues are quickly addressed by an OB/GYN with specialized training in those situations. For patients without a primary obstetrician at the hospital, the OB hospitalist cares for the patient from arrival through discharge. For patients whose obstetrician practices at the hospital, the OB Hospitalist addresses the emergent situation with which the patient presents and then coordinates continuing care with her primary obstetrical clinician.

The nucleus of this model is that the nurse and hospitalist work together to triage and take a team- based, “first touch” approach to presenting patients in the OBED. This ensures that the patient begins on a care path that has more effective communication, timely intervention, and proactive identification of potential issues. It helps to eliminate the silos that can lead to harms in care.

A recent study conducted with Ascension Health, the largest non-profit health system in the U.S., offers empirical evidence that this “first touch” model may provide significant benefit in reduction of serious harm incidents. The case study examined the key risk mitigation strategies that resulted in favorable loss trends / claim reduction for the organization in recent years; the researchers supported their analysis with Willis Towers Watson’s National OB benchmarking study of >550 birthing hospitals.

The analysis found that the health system experienced lower claim frequency, and lost cost per birth, than average industry trends found in the benchmarking study, and identified the use of OB hospitalists at their hospitals as a valuable best practice initiative in driving down the loss. Specifically, the analysis identified a 31 percent reduction in serious harm incidents before and after implementation of OBED programs.

A deeper look at PSO and the Ascension data suggests that this “first touch” OBED approach reduces harms because it is structured to lower the potential for harm. Under the OBED model, most patient encounters in Labor & Delivery begin with assessment and triage by an OB/GYN hospitalist. Even if an OB hospitalist is not involved in the delivery, or ultimate co-management of patient, the harm data suggests that it is the early team-based involvement and assessment of the patient that is critical in reducing harm from occurring during their labor and delivery.

A 2015 study by researchers at Northwestern University found adverse events or potential adverse events occurred in approximately 1 in 5 women admitted to a labor and delivery unit.[3] Up until the last few decades, mitigation has focused on improving the practice of medicine – a critically important effort, but one that PSO data tells us must be coupled with transformation of the Labor & Delivery environment. The World Health Organization’s 2012 Every Woman, Every Child (EWEC) Innovation Working Group (IWG) report notes that, “Much of healthcare and health-systems based research has focused on pioneering new science. More recently there has been a focus on services already in place — specifically, investigating how to minimize harm in existing health systems and understanding better how current healthcare practice can be made to be as effective and efficient as possible.”

It would be welcome irony if the impersonal “adverse event” was eliminated by focusing on the most personal aspect of the delivery of perinatal care: a clinical “first touch.”

References

- The Doctor Company, 2007-2013 Malpractice Claims

- https://www.acog.org/Clinical-Guidance-and-Publications/Committee-Opinions/Committee-on-Patient-Safety-and-Quality-Improvement/The-Obstetric-and-Gynecologic-Hospitalist

- The frequency of and factors associated with adverse events on labor & delivery Chadha, Angad et al. American Journal of Obstetrics & Gynecology , Volume 212 , Issue 1 , S63

Healthcare – An Industry Unlike Any Other Goes Global

Lilac Nachum, PhD, City University New York, Baruch College [1]

Contact: lilac.nachum@baruch.cuny.edu

Abstract

What is the message?

How the balance between the global and the local is transforming the scope of opportunities and raising challenges for healthcare professionals and institutions.

What is the evidence?

This paper is derived from a course on the globalization of healthcare developed and taught by Professor Nachum as part of Baruch College MBA program for Healthcare professionals. It is based on a variety of secondary sources and was informed by class discussions with the healthcare professionals enrolled in the course

Submitted: March 19, 2018; accepted after review: June 15, 2018

Cite as: Lilac Nachum. 2018. Healthcare: An Industry Unlike Any Other Goes Global. Health Management Policy and Innovation, Volume 3, Issue 2.

The Globalization of Healthcare

The healthcare industry[2] has been transformed in recent years from what was traditionally a primarily domestic industry into an increasingly global industry, defined by cross-national principles. In parallel to the forces that have driven the globalization of the industry, however, there have been others that have resisted these developments and anchored the industry in national systems of healthcare delivery and consumption. This interplay between the global and the local is emerging as a predominant feature of the industry that is shaping its contemporary dynamics and will have significant consequences in the years to come. In this paper, I seek to explicate this development and examine the opportunities and challenges that it holds for healthcare providers and the policymakers who oversee the industry.

Healthcare: An Industry Unlike Any Other

The healthcare industry is distinctive in at least three ways. For one, in contrast to most other industries in which the ultimate goal of firms is profit-maximization, in healthcare this goal often poses a challenge to value creation through quality care. As an industry whose value creation lies in extending lives and enhancing their quality, there is a strong moral dimension attached to value creation, producing a delicate balance between this imperative and the different and often conflicting demands of economic performance and survival. Notwithstanding notable successes in combining value creation with financial goals, these goals often conflict with each other and impose tradeoffs. The vague notion of what is to be maximized challenges the development of performance measurement and creates scope for different points of view as to the appropriate indicators that should be used.

Further, the industry is characterized by distinctive structural issues. The consumers – patients with symptoms – are typically ignorant about the cause of their symptoms and the required treatment for relieving them; the suppliers – healthcare professionals, in affiliation with healthcare institutions or on their own, who diagnose the cause of the symptom, prescribe the treatment and may implement it – are, at least in the developed world, typically not paid by the consumers. Rather, market transactions involve one and often more intermediaries who administer the payment.[3] These intermediaries themselves vary in terms of their goals, agency and power, and their impact on the engagement between the healthcare provider and the patient receiving treatment.

Lastly, the healthcare industry stands out in terms of the demand for its output. Given the complex structure of the industry, identifying the actual source of demand is a challenge as it includes the patient, the doctor who prescribes the treatment and may implement it, and the payer for the service (at least in countries where the payers and the customers are two separate entities). Demand is often inelastic (what is the monetary value of life?) and is prone to information asymmetries of numerous kinds that influence the transactions and place much power in the hands of the intermediaries who pay for the service.

The distinctive attributes of the healthcare industry assume additional complexity as the industry globalizes. The ambiguity regarding the ultimate goal of healthcare, along with the subsequent difficulty of devising corresponding performance measures (notably whether performance should be measured by financial indicators, quality of care, outcome of treatment, or other metrics), are magnified by country-specific philosophies of life and mortality and varying perceptions regarding universal access. The United Nations (UN) Universal Declaration of Human Rights has long declared access to healthcare a basic human right: ‘everyone has the right to a standard of living adequate for the health and well-being of himself and of his family, including food, clothing, housing and medical care’.[4] Although more than half a century old, this assertion has not been adopted by all countries that are members to the UN in a comprehensive way. Variations in moral philosophy surrounding healthcare and the extent to which it is seen to be a universal right introduce stark differences in the healthcare industry across countries. These variations are reinforced by varying views of human ability to influence life quality and longevity versus those of faith and religion, including different perceptions of the value of life itself.

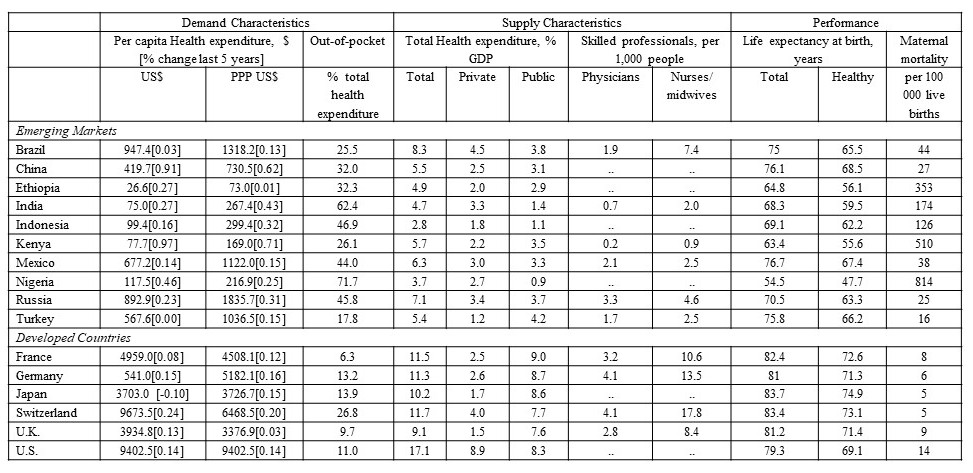

These philosophical and cultural differences bring about varying views as to who should be responsible for healthcare provision and who should pay for it. The UN International Covenant on Economic, Social and Cultural Rights assigned the responsibility for the provision of healthcare to national governments: ‘[every nation is responsible for] ‘the creation of conditions which would assure, to all, medical service and medical attention in the event of sickness’. [5] But this declaration has not been universally practiced. The size adjusted government expenditure on healthcare varies enormously across countries (Table 1). Country-specific approaches differ in terms of the ultimate provider and payer for healthcare, whether private or public, or as is the case in many developing countries – by the consumers. There are also considerable country differences in terms of access to healthcare services and its coverage. As the data in Table 1 show, out-of-pocket payment accounts for up to three quarters of total healthcare expense in countries such as Nigeria and India, but represents around a tenth or less of the total in many developed countries. These variations are accentuated by differences in the level of economic development and that affect the availability and quality of services (Table 1).

Table 1. Selected Healthcare Indicators by Country

Latest available: 2014-2016

WHO, World Health Statistics http://who.int/entity/gho/publications/world_health_statistics/2017/en/index.html; World Bank Development Indicators Database

Country differences also express themselves in the nature of demand. Varying perceptions of healthcare versus healing by forces of faith and religion, coupled with different views of modern versus traditional medicine, often determine the level of demand for healthcare services and its nature. In addition, education levels influence information asymmetries between participants in the complicated transactions that define the industry. Lastly, differences in life style, diet, and other ongoing activities affect the types of diseases prevalent across countries and their frequency.[6] The data in Table 1 show vast variations in per-capita healthcare expenditure, indicative of these differences in the demand for healthcare across countries. In the following sections I discuss how the tension between the global and the local is shaping the nature of supply and demand for healthcare around the world.

The Tension between the Global and the Local: Demand and Supply for Healthcare Services

The forces that are driving the healthcare industry to become increasingly global and those that connect it to national systems manifest themselves within the framework described above. They are apparent in relation to both the demand for healthcare services and its supply. On the one hand, major participants in the healthcare industry, including healthcare professionals and institutions, drug producers, and consumers, have become more mobile, drawing healthcare delivery and consumption into global networks of interactions. At the same time, cultural, institutional, and behavioral differences continue to anchor the industry to different countries and arrest globalization.

Global and Local Demand

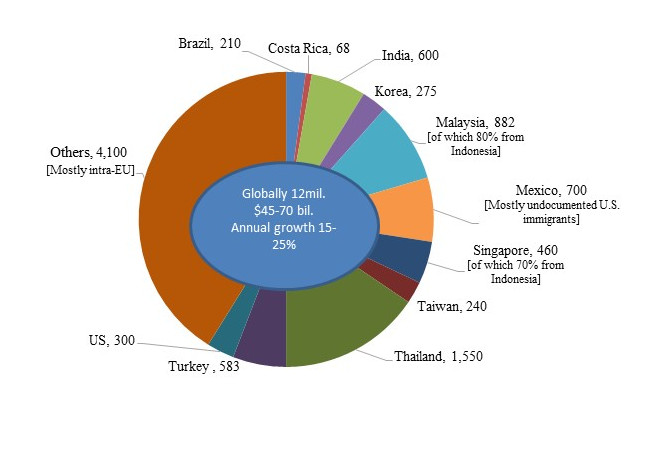

A major development that has globalized demand for healthcare is what has come to be known as ‘medical tourism’, that is, the travel by patients for medical treatments to other countries. While this phenomenon has existed for decades and by some accounts centuries, until recently it was small and confined to wealthy people from developing countries traveling to Western countries for medical treatment. What is new is the recent emergence of medical tourism from developed countries to emerging markets (Figure 1), driven by the development of local healthcare institutions in emerging markets and improvement in the quality of their healthcare services.

Figure 1. Medical Tourism

Destination countries by number of patients (in thousands), 2015

Patients Beyond Borders, http://www.patientsbeyondborders.com/medical-tourism-statistics-facts

Based on estimates by Deloitte, McKinsey, Gallup, the Economist, host countries health and tourism ministries

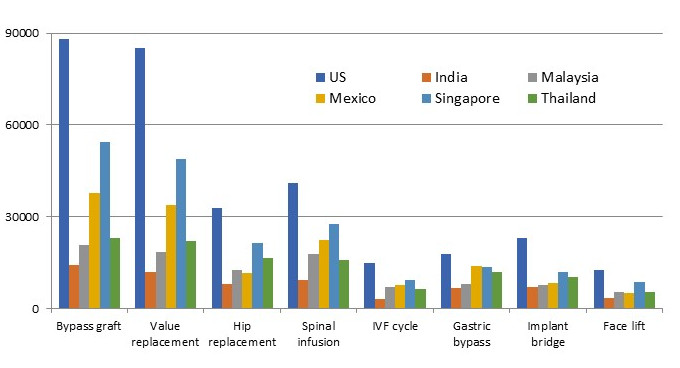

These institutions offer medical services for a fraction of the costs in developed countries (Figure 2) and minimal waiting time.[7] Combining a low-cost labor force with efficient delivery, assisted by state-of-the-art technology, hospitals in emerging markets have managed to cut costs and shorten delivery time to levels unimaginable in the developed world.[8] Accreditation by U.S. and Global Accreditation Associations provides quality assurance for patients and payers, and have removed major obstacles for the growth of medical tourism. By 2016 more than 600 hospitals worldwide were accredited by the Joint Commission International Accreditation, a number that has been growing by about 20% annually[9]. In 2015 medical tourism amounted for an estimated $40-$75 billion worth of economic activity, or about 1% of global healthcare expenditure.

Figure 2. Cost Variations of Medical Procedures

US$: 2015

Patients Beyond Borders

The development of medical tourism has captured the attention of healthcare insurance services in the developed world. Large U.S. insurers have examined these offshore developments as low-cost alternatives for U.S. services, and some have incorporated them in their offerings. Britain’s NHS is considering partnerships with leading players in India and Thailand as a way to cut waiting times.

The growth in medical tourism suggests that at least in the short term, it offers solutions to limitations of healthcare systems in developed countries (i.e., high costs in the U.S. and long waiting lists in Europe). The long-term impact of this development on progress in addressing the causes that generate the demand for medical tourism is unclear. It appears likely that in the mostly privately-owned U.S. industry, competition from low-cost alternatives would create pressure for increased efficiency and lower costs, as I discuss in some detail below. This in turn could reduce demand for low-cost solutions elsewhere. The response of the government-owned healthcare system is Europe is more difficult to predict, as it less likely to be subject to market forces. European governments may opt for using medical tourism as a low-cost alternative that enables reduction of government resources allocated for healthcare rather than adding capacity to their local industries.

At the same time that demand for healthcare continues to expand globally, the type of demand varies significantly across countries, reflecting for the most part country variations in the prevalence of diseases. For instance, the number one cause of death in the developed world is heart disease, accounting for more than 12% of total deaths, whereas in mid- and low-income countries most deaths are caused by cerebrovascular disease (14%) and respiratory infections (11%).[10] Likewise, the incidence of cancer is three times higher in China than in India. The disparity in Africa is even greater.[11]

Global and Local Supply

On the supply side, the major providers of healthcare, notably healthcare professionals, hospitals, and pharmaceutical and other med-tech companies, have vastly broadened their global reach in recent decades. Movement of healthcare professionals, predominantly from emerging markets to developed countries, is not new, but its magnitude has grown considerably, fostered by reduction in traveling costs and liberalization of immigration policies for healthcare professionals. Initially, nurses came most commonly from the Philippines, but more recently, their national origins have widen considerably.[12]

These developments have often been driven by mismatches between supply and demand that have proliferated around the world – according to the World Health Organization (WHO) by more than seven million healthcare professional providers in 2016, a number that is estimated to double by 2035. More than two-third of the 300 respondents to the American College of Healthcare Executives’ annual survey reported experiencing shortage of registered nurses and primary care physicians, and more than half noted shortage of specialized physicians.[13] Leading U.S. hospitals have been importing nurses since the 1980s in the face of a large nursing shortage.

The movement of doctors across countries has also been prevalent, although less common than that of nurses due to different qualification requirements. According to one estimate almost 40,000 Nigerian doctors practice outside Nigeria, three-quarter of them in the U.K.[14] Whereas for the most part, these moves are initiated by individuals seeking to further their careers and better their lives, in some cases they are assisted by governments. For instance, the Cuban government, under the auspices of the WHO, exports local doctors to Brazil, pays their salaries, and receives payment for their services from Brazilian authorities, turning these transfers into a major source of the government’s foreign currency.[15]

Industry has a longer track record of global expansion. Pharmaceutical companies, in particular, have long been global. The high cost of drug development that gives rise to vast scale economies, coupled with short spans of patent protection, have pushed pharmaceutical companies to expand the market for their drugs across the globe.

Most recently, hospitals, which were traditionally deeply grounded in particular localities, also have started to globalize. Leading hospitals in emerging markets are rapidly expanding overseas. India’s Apollo Hospitals Group, the largest private hospital group in Asia, operates 55 hospitals with 9,215 beds, and has facilities in India, Sri Lanka, Bangladesh, Ghana, Nigeria, Mauritius, Qatar, Oman, and Kuwait, and plans for further global expansion. Only regulations have prevented it from entering the U.S. [16]. Some of the most prestigious U.S. hospitals, among them Johns Hopkins, Cleveland Clinic, Harvard, and Duke, have formed partnerships that offer combined treatments in the U.S. and overseas. Similarly, Canadian hospitals such as SickKids Children’s Hospital have begun to expand internationally.

The major barrier for the globalization of healthcare supply is country regulations. Doctors are tied to the locality in which they receive their medical training by varying qualification requirements that raise the cost of movement across countries. Foreign hospitals’ expansion is also limited by country restrictions, making this segment of the healthcare sector the least global. The share of FDI in healthcare services is a fraction of total service FDI in both developed and developing countries, although it registered substantial growth over the last decade. In an era where cross-border M&A activity has been mushrooming across industries, there has been almost no cross-border acquisitions of hospitals (although domestic mergers are common).[17]

U.S. hospitals and other healthcare providers have been among the world’s most active foreign investors, particularly in Latin America and the U.K.[18]. The Federation of America Hospitals lists almost a hundred overseas hospitals owned by U.S. major hospitals. However, there is no corresponding activities the other way around. For instance only regulations prevented Indian hospitals from establishing themselves in the U.S. Whereas countries around the world, most notably developing countries, have become increasingly open to foreign ownership of healthcare services, the U.S. has been highly restrictive.

Regulations and country variations have been a drag also on the global expansion of pharmaceutical companies. The regulatory environment that surrounds drug development, testing, and approval varies considerably around the world, undermining advantages of global scale. Varying levels of patent protection across countries are another challenge for the globalization of pharmaceutical companies, and variations in diseases and their prevalence impact global standardization of drug development.

Implications for the Healthcare Industry

As the home of some of the world’s most prestigious hospitals and healthcare professionals, developed country institutions and professionals are well-positioned to benefit from the globalization of the healthcare industry. Global developments increasingly make it possible to scale the reputation of hospitals and professionals globally and exploit them on a global scale. It enables local institutions in these countries to attract patients from around the world to their existing facilities and increase their share of the rapidly growing medical tourism. As emerging market consumers become wealthier, demand for high quality healthcare services in these countries is increasing, and could foster medical tourism to developed countries.

In addition to attracting patients to developed countries, these constituencies should also be able to expand their scope globally by establishing themselves overseas, by either direct investment or through various forms of partnerships with local providers in foreign countries. This process will vary according to the type of services provided and their comparative advantage in different countries.

Some reputable U.S. hospitals have recently been experimenting with such endeavors, and would likely pursue these further as a means to leverage on their expertise and increase market share. The Directory of U.S. Hospital Partnerships with Foreign Hospitals, published by the American College of Healthcare Executives and the American Hospital Association, lists dozens of partnerships. To qualify for inclusion in the Directory, partnerships need to be deep and comprehensive, and form ‘a cooperative and mutually beneficial relationship between a U.S. hospital and a hospital in a different country, … designed to facilitate the exchange of knowledge, technical information and other insights that contribute to improved healthcare services in both hospitals.’[19]

At the same time, global developments could also pose considerable challenges to hospitals and healthcare professionals in the developed world. The forces that enable them to broaden the potential market for their services also increase cost pressures and put them in competition with low-cost providers. These constituencies, notably in the U.S., have little experience in cost-driven competition and this could pose a serious challenge for them. The strongest impact of these forces will probably be felt in what are today the most lucrative parts of the industry, namely the highest cost operations and procedures. The high cost of these treatments compared to the emerging alternatives overseas will increase the incentives to travel elsewhere. These developments will put pressure to improve the consumer experience (for instance, by providing rehabilitation facilities for medical tourists and accommodation for accompanying relatives) and at the same time cut costs in order to stay competitive.

The challenge for these constituencies lies in designing strategies that are responsive to the tension between the global and the local that I outlined in this paper, and take advantage of them by articulating the appropriate balance, considering their distinctive sources of strengths and weaknesses. The rewards for doing this properly are vast.

References

- This paper is derived from a course on the globalization of healthcare developed and taught by Professor Nachum as part of Baruch College MBA program for Healthcare professionals. An earlier version of this paper appeared as Baruch College’s Weissman Center Occasional Paper, 2018. The author acknowledge with deep gratitude the excellent comment of the Editor during the review process.

- The health care industry is defined broadly to include health care professionals (e.g., doctors, nurses), healthcare institutions (e.g., hospitals), pharmaceutical companies, and producers and suppliers of equipment for healthcare.

- This is the common practice in developed countries. In developing countries large share of healthcare costs is covered by the consumers, as will be discussed below.

- Article 25, 1948

- Article 12, 1966